Corporates, corporates and more corporates…

We have seen strong growth in the demand for alternative credit to sit alongside traditional fixed income to boost returns and diversify risk. Asset owners need to be discerning when building portfolios to ensure they are not overloaded on corporate exposure or undue concentration risks. Most credit portfolios typically hold substantial corporate exposure – often with overlapping issuers – across developed-market investment grade and high-yield bonds, leveraged loans and emerging-market corporate bonds. Furthermore, the sprawling securitized credit and private debt asset classes also carry ample corporate exposure, with a few clear examples highlighted below:

- Direct lending to corporate borrowers has seen significant growth for a number of years and has generally been an asset owner’s first step into private credit. The upper middle-market portion of the direct lending market is now large enough to compete with leveraged loans, with many issuers arbitraging between the two markets.

- Collateralized loan obligations (CLOs) are the largest part of the non-agency securitized credit market, with the underlying assets being comprised of corporate leveraged loans. Here, too, a portfolio of CLOs can introduce more overlap across borrowers and may offer less diversification than expected.

- Significant Risk Transfers (SRTs) are a smaller but growing asset class, which sits within both the private debt and securitized credit investment universes. SRTs finance the “reinsuring” of balance sheet assets for banks, with most asset pools primarily linked to corporate loans.

Why is this an issue? A high concentration of underlying corporate risk leaves asset owners at risk of higher correlations with equities. While debt backed by sovereigns, consumers and real assets will inevitably track economic cycles to a degree, these assets can provide attractive long-term results and can offer a much-needed ballast when corporates are under pressure.

Where to look for diversification?

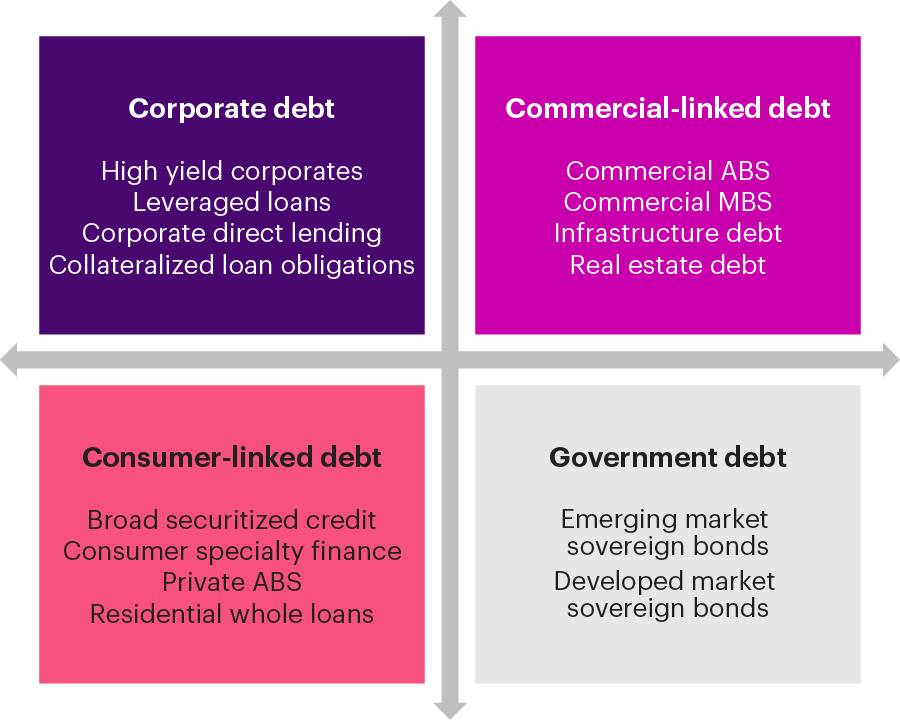

While the aforementioned asset classes are important components within a return-seeking credit strategy, asset owners should also prioritize these non-corporate-linked risk profiles:

- Consumer-linked debt: Securitized credit strategies provide exposure to a variety of different collateral, including consumer mortgages, auto loans, student loans, and other esoteric consumer loans. Many of these are floating rate and offer strong income, akin to CLOs or leveraged loans, offering insulation against interest rate volatility. Additionally, residential whole loans can be accessed through private markets.

- Commercial-linked debt: This broad group includes commercial mortgage-backed securities (MBS) and asset-backed securities (ABS) tied to non-consumer sectors like data centers, aircraft, pharmaceutical royalties, shipping containers, and telecom towers. This type of diversification can also come from private loans against real assets, real estate, and infrastructure.

- Government debt: Emerging-markets sovereign bonds can offer important duration, curve, and currency diversification to a corporate-heavy portfolio and more attractive yields than developed-market government bonds. While some emerging-market exposure can be accessed through the corporate bond market, we believe rates and currency management is a different skill set from credit selection and better accessed through specialist mandates.

What does a well-diversified credit portfolio look like?

We believe a robust credit portfolio is diversified across corporates, consumer and commercial-linked debt, and government bonds. Against this backdrop, there are many paths to achieve a successful outcome. Asset owners can choose from a wide variety of mandates within each universe to achieve their goals while also meeting their credit risk tolerance. For example, some consumer-linked ABS mandates focus more on residential mortgages, whereas others focus on less-liquid, lower-rated esoteric assets – both come with different risk and return profiles.

There are other factors to consider when assessing how to improve diversification. Geography, public versus private debt, and vintage diversification in private markets are additional avenues. Manager diversification is also an important factor to consider when it comes to investment style and risk and reward preferences.

How should asset owners assess their portfolios?

We believe asset owners can build more robust and resilient portfolios through careful construction of their credit allocations. They should take special consideration when thinking about the underlying risk exposures and take advantage of the various non-corporate-linked securities that only credit can provide. While spreads have come in across most credit markets as of late 2025, many pockets of value do still exist. Asset owners need to be dynamic when constructing their portfolios to take advantage of these opportunities and use the full spectrum of the universe available to them.

Whether you are looking to invest in alternative credit for the first time or looking to review your allocations in this new environment, we believe WTW has the experience necessary to partner with you. At WTW, we have a team of dedicated liquid alternative credit and private debt specialists who have helped our clients with selecting highly skilled managers, building highly diversified portfolios over time, and investing at scale. We have a proven track record of innovating with credit managers to design new and creative solutions to address our client’s ever-changing needs.

Disclaimer

This document was prepared for general information purposes only and does not take into consideration individual circumstances. The information contained herein should not be considered a substitute for specific professional advice. In particular, its contents are not intended by Towers Watson Investment Services, Inc., and its parent, affiliates, and their respective directors, officers, and employees (“Willis Towers Watson”) to be construed as the provision of investment, legal, accounting, tax or other professional advice or recommendations of any kind, or to form the basis of any decision to do or to refrain from doing anything. The information included in this presentation is not based on the particular investment situation or requirements of any specific trust, plan, fiduciary, plan participant or beneficiary, endowment, or any other fund; any examples or illustrations used in this presentation are hypothetical. As such, this document should not be relied upon for investment or other financial decisions and no such decisions should be taken on the basis of its contents without seeking specific advice. Willis Towers Watson does not intend for anything in this document to constitute “investment advice” within the meaning of 29 C.F.R. § 2510.3-21 to any employee benefit plan subject to the Employee Retirement Income Security Act and/or section 4975 of the Internal Revenue Code.

This document is based on information available to Willis Towers Watson at the date of issue and takes no account of subsequent developments. In addition, past performance is not indicative of future results. In producing this document Willis Towers Watson has relied upon the accuracy and completeness of certain data and information obtained from third parties. This document may not be reproduced or distributed to any other party, whether in whole or in part, without Willis Towers Watson’s prior written permission, except as may be required by law.

Views expressed by other Willis Towers Watson consultants or affiliates may differ from the information presented herein. Actual recommendations, investments or investment decisions made by Willis Towers Watson, whether for its own account or on behalf of others, may differ from those expressed herein.