In this article from the 2025 Energy Market Review, we share observations and outlooks on the insurance upstream energy insurance market, alongside actionable insights to help companies put themselves in a strong negotiating position when taking their risks to market.

At a glance: Upstream energy insurance market trends

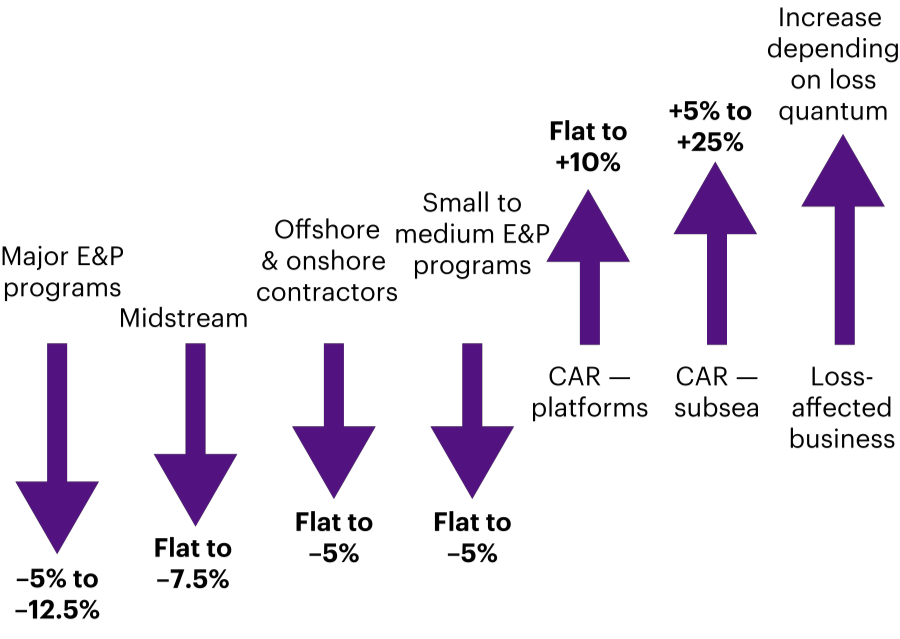

- Softening market conditions have accelerated beyond predictions for the most attractive elements of the upstream portfolio.

- Capacity continues to climb and more underwriters are willing to take on leadership roles, driving pricing down.

- Insurers are under continued pressure to grow their market share, putting pressure on signings even when core business is placed at a significant reduction.

- For upstream insurers, the traditional follow-only role is hard to play. An uptick in quoting markets, alongside the resurgence of broker facilities, means that remaining competitive is more important than ever.

- Placements with significant premium volume continue to provide the most opportunity to generate larger rating discounts.

- The premium pool continues to dwindle, only supplemented by construction, but remains small in comparison to the exposures being insured, putting the sustainability of reductions under question.

- Alongside major construction losses, attritional losses have the potential to further deteriorate profitability despite the absence of large market-changing losses within the last 12 months.

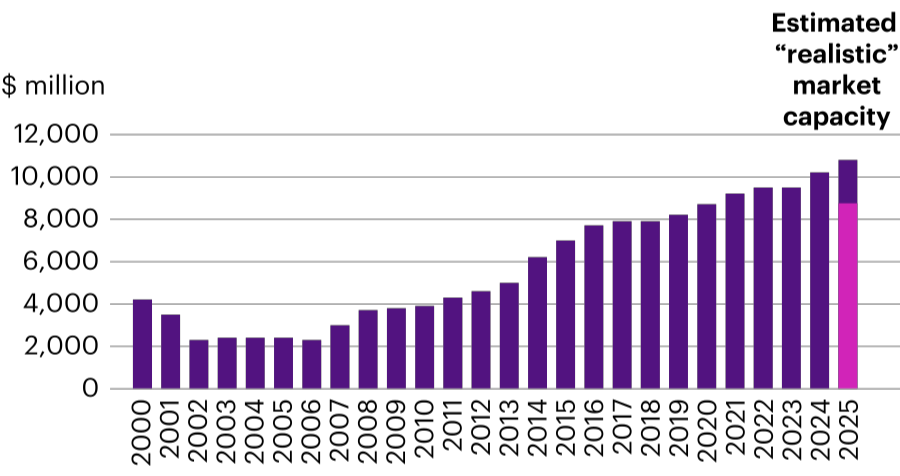

Upstream capacity continues to climb

While there are no significant new entrants to the market, pressures to remain relevant and grow market share have added additional capacity of c.$275 million from existing markets, contributing to a general c.5% growth in capacity from last year.