Chapter five of the FTSE 350 DC Pension Survey 2021

It is reassuring to note that sponsors are committed to improving retirement outcomes for employees, with this being the highest priority area for those companies surveyed. Respondents plan on achieving this objective through enhancing the support available at retirement, with some 59% giving this as a priority for the next two years, a significantly higher number than in last year’s survey.

In part, this may be a response to the pandemic, which has highlighted the importance of having the right level of at-retirement support in place for members to help them make well-informed decisions at the right time.

Note: “Don’t know” was excluded.

Source: FTSE 350 Defined Contribution (DC) Pension Scheme Survey, 2021

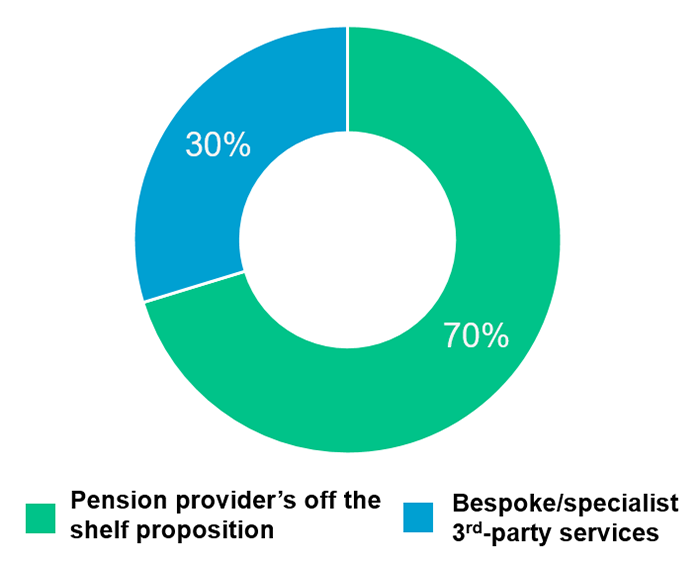

There is heavy reliance on providers’ off-the-shelf retirement propositions with some 70% of respondents relying on them. While this is entirely understandable where members are paying for that support through the scheme’s charges, it is still important for sponsors to ensure that the proposition is adequate for its needs and to look for areas where further enhancements could be sourced elsewhere. If a provider doesn’t offer support, or if that support is limited to the provider’s own products, this service can be provided separately via a third-party.

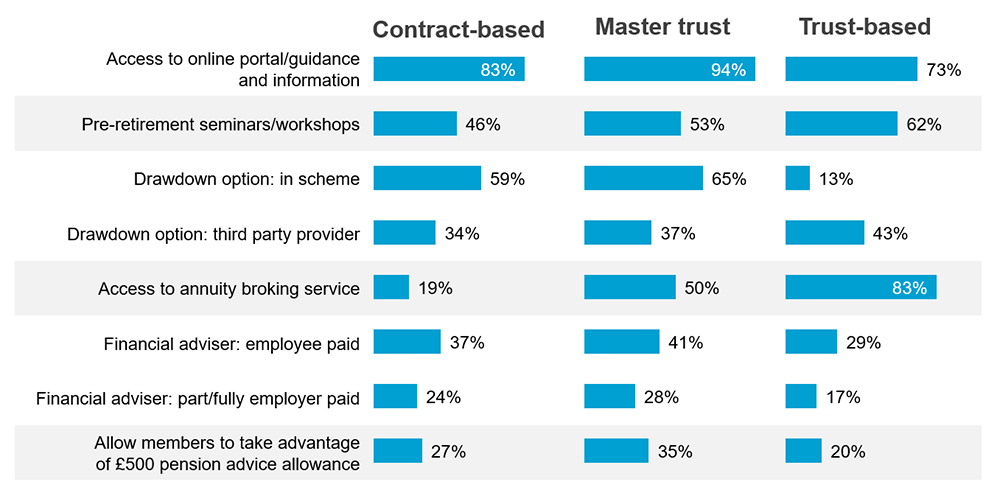

Trust-based schemes show high use of annuity broking services (83%), whereas fewer (50%) offer access to a drawdown option. Not surprisingly, given the complexity of managing drawdown options in-house, the most common option for trust-based members was provision via a third party (43%). The numbers using a third-party drawdown provider have continued to increase from last year’s survey and this is a trend we expect to continue as sponsors seek to fill in gaps in their support.

An increasing number of contract-based and master trust providers have developed drawdown solutions with the result that these arrangements now have high levels of access to drawdown options, the majority in-house. This can be convenient for members, though it remains important for sponsors to be satisfied that their chosen provider remains suitable for the drawdown option as well as during the accumulation phase.

Source: FTSE 350 DC Pension Scheme Survey, 2021

Despite the growth in digital support and guidance it is recognised that many employees still value financial advice when it comes to making retirement decisions. Across the survey, almost a quarter of participants partially or fully fund access to an adviser while 35% offer access where the employee pays. Providing access to advice and guidance at retirement can be extremely valuable as members navigate an array of options and tax implications. This can complement the provision of access (or facilitated access) to the full suite of options available to members at retirement.

Only about a quarter of participants allow members to take advantage of the £500 pension advice allowance. As this is a no-cost option for employers and tax efficient for members, it is perhaps surprising that take up remains stubbornly low. In part this is down to providers not offering the functionality, but it is also hard for advisers to deliver holistic retirement advice at that level of fee. Nevertheless, provision of advice has been given a boost by the recent TPR/FCA guidance for employers and trustees on providing support with financial matters without needing to be subject to FCA regulation. This provides welcome clarity on what sponsors can and can’t do.

Overall, we can see that sponsors have already made progress in supporting members at retirement and they remain committed to continuing to improve the offering. As this is personal to each scheme and its membership, we expect that sponsors will look to identify the gaps they face in their provision and seek to plug in solutions that meet their needs and budget. Measuring the effectiveness of the support will also help sponsors satisfy themselves that this is a contribution towards improving member outcomes.

| Title | File Type | File Size |

|---|---|---|

| FTSE 350 DC Pension Survey 2021 | 4.9 MB |