How to find the manager with the right style for you

In September 2017, the Competition and Markets Authority (CMA) launched its market investigation into the supply and acquisition of investment consultancy and fiduciary management services, in response to an earlier Financial Conduct Authority (FCA) study on the asset management industry. Now that the CMA review has concluded, Lok Ma and Aman Hanspal describe the main findings, as well as some related developments in the rapidly expanding fiduciary market.

The CMA looked at how investment service providers and asset managers competed to deliver value, including the extent to which they were willing and able to control cost and quality along the value chain. Whilst some headlines seemed to imply this was all about fiduciary managers, in reality the role of investment consultants also fell within the scope of the review.

Overall, the CMA found an industry that was functioning well, with no excessive concentration or high barriers to entry. There was also no evidence of firms seeking to introduce fiduciary management where this was not in the client’s best interest. This ultimately meant that investment consultants could continue to operate more or less as they were, and it was not deemed necessary for firms to split up their fiduciary and consulting businesses.

The CMA did, however, identify a number of areas for improvement.

The final CMA order is expected to be published in June this year, after which the remedies will start coming into force.

Over the course of last year, whilst the CMA review was still ongoing, there was a slowdown in fiduciary manager appointments as trustees awaited the outcome. As the dust settles, however, there are clear signs that the number of competitive fiduciary appointments is back to growing at an accelerating rate. More and more trustee boards are now deciding to delegate the day-to-day management of their investment portfolio, to focus more on the key strategic decisions that have the greatest impact on the benefit security for their members.

As the fiduciary management market continues to expand and develop, we are seeing greater differentiation between mandates: in terms of the trade-off between cost and sophistication, and in terms of the types of assets and financial instruments used to generate returns and manage risk.

During the (now compulsory) competitive tender process when first appointing a fiduciary manager, trustees will therefore need to consider the relative merits of these different investment styles, and select a provider that most suits their own objectives and beliefs. In light of this, the role of professional intermediaries is likely to become ever more important in the investment services market. An intermediary is an independent third party employed by the trustees to help with the various stages of a tender such as drawing up the initial shortlist of providers, framing the right questions to ask, and assisting the trustees in their ultimate decision. A good intermediary will have carried out extensive research into the various providers, and be able to provide a fair and impartial view – the focus should be on providing information and facilitating the trustees’ decision-making process.

At an early stage of a selection exercise, a well-run tender will aim to match the trustees’ investment beliefs with the solution. By ‘investment beliefs’, we are referring to a set of working assumptions and thoughts about the investment world - an example might be that ‘a good active manager can (or cannot) increase returns after allowing for fees’. The beliefs should capture a consensus across the trustee board, and provide the foundation on which trustees make their decisions. It is important that the shortlisted fiduciary managers employ a style that is compatible with these beliefs.

Often the trustees will need to consider the trade-off between competing desires, for example, minimising cost is clearly a good thing, but so is accessing a wide range of return sources to reduce concentration risk. Coming up with a set of workable investment beliefs can therefore involve prioritising some needs over others.

As an illustration of how this might work in practice, the below sets out how our range of fiduciary management services are tailored to trustees with different priorities:

| Trustee investment beliefs / circumstances | Fiduciary management approach | |

|---|---|---|

| Adopt most efficient portfolio, with focus on achieving optimal net-of-fees results | → | Best ideas approach: including highest rated active managers and investment in illiquid assets to enhance returns |

| Value the risk management benefit of a broad spectrum of return sources | → | Core diversified approach: including significant allocations to investments with low correlation to the main equity and bond markets |

| Greater emphasis on using traditional market exposures and managing costs | → | Core approach: smart indexation for equities and a diversified portfolio for bonds, alongside a downside protection strategy |

| Manage risk for a well-funded, maturing scheme, possibly on its way to settling liabilities | → | End game approach: low-risk cashflow driven investment (CDI) or run-off strategy, incorporating insurance transactions (e.g. pensioner buy-in) where appropriate |

In addition to the above, the trustees should also develop their beliefs around the importance of environmental, social and governance (ESG) factors, and the degree of flexibility in adapting the portfolio when market conditions change. How each fiduciary manager incorporates these into their portfolios and approaches will also differ.

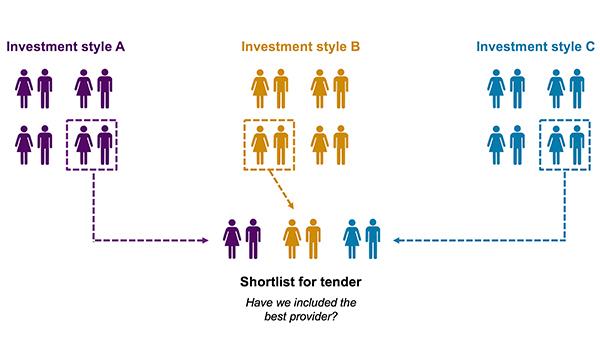

In choosing the right fiduciary manager, we think it is more helpful for the trustees to work out their beliefs first, and identify providers with solutions that are consistent with these beliefs, at the shortlisting stage. The traditional approach - of lining up stylistically very different managers in a final pitch - may result in a provider being appointed that has the right style but is not the best of its ilk. The good news is that we are increasingly seeing the new approach being adopted.

Overall, the improved transparency brought about by the CMA review, combined with a thoughtful competitive tender process based on alignment with investment beliefs, should mean that trustees can be even more confident of appointing the fiduciary manager that is best placed to implement their chosen investment strategy.