At face value the investment strategy of an insurer is similar to that of a pension scheme seeking to achieve a low risk run off of its liabilities. However, an insurer is subject to greater restrictions than a pension scheme.

An insurer’s investment strategy must balance the competing demands of:

Bulk annuity providers in the UK are supervised by the Prudential Regulatory Authority (PRA) and the amount of capital that they are required to hold is determined by the European regulation, Solvency II, which was introduced from 1 January 2016.

At a high level, insurers are required to hold sufficient capital to meet all of their obligations to policyholders over the next year with a 99.5% probability (in practice most insurers hold significantly more capital than this). Or, in other words, they must have the ability to withstand a 1-in- 200 shock event.

By investing in low risk assets which provide a close match to the liabilities, the insurer is able to minimise the level of capital they hold, and offer the customer (in this case the pension scheme) a better price, whilst achieving a higher level of return for their investors.

Investment in low risk assets helps, on the one hand, to minimise capital requirements, but such assets are typically characterised by lower rates of return. The lower the expected rate of return used to discount scheme cash-flows, the higher the premium charged; so the competitive advantages gained from optimisation of the capital position may be lost.

Insurer investment strategy is therefore driven by the need to optimise capital requirements by seeking assets to provide a precise liability match, whilst generating as much return as possible from low risk assets.

Insurer investment strategy is underpinned by the pricing process for bulk annuities.

The first stage of the pricing process is for the insurer to project the expected cash-flows underlying the buy-in contract. The insurer will then build an asset portfolio that is expected to deliver those cash-flows with a very high degree of certainty.

The approach taken by pension schemes is similar, however the precision of the matching is perhaps considered less important - small movements, say from a duration mismatch, may be acceptable to a pension scheme that can revert to its sponsor for additional funding.

At the next stage the insurer uses a combination of immediately accessible low risk investments as building blocks to best match the cash-flows. The objective is to achieve close matching using the income from these assets, at the highest yield possible. This process is relatively easy for the earlier years – say the first 20 – where a combination of high quality corporate bonds and swaps can be structured to give yield and also meet the cash-flows.

It becomes more challenging beyond this period, and remember a typical pensioner buy-in can have cash-flows stretching out over 50 years. To the extent that insurers are forced to use gilts to match these later cash-flows, the overall expected return from the portfolio is reduced and in turn, the buy-in premium increased.

To address this poor yield, insurers have increasingly sought to source ‘Secure Income Assets’ or ‘SIAs’ to provide longer duration matching. These are assets with contractual, inflation linked (RPI or CPI), long-term cash-flows with robust counterparties and/or collateral backing. Most of their value is derived from the cash-flows themselves.

Examples of such assets used by insurers recently include equity release products, mortgage backed securities, social housing, solar, wind farms and airport landing slots. Much of the additional yield associated with these assets comes from the illiquidity premium – which the insurers are very happy to benefit from because they have such long-term liabilities.

These assets, whilst growing in availability, are still relatively difficult to source and there is considerable competition for them. Whilst getting an asset of the size and characteristics that exactly matches the long term characteristics for an individual pension scheme’s buy-in is challenging, in a number of cases insurers have been able to negotiate bespoke terms such that the income stream meets their matching needs.

In an example of this, we recently helped one pension scheme enter into a monitoring period with an insurer with a highly aggressive target premium (around £300m). Over a period of months the insurer sought to negotiate and acquire the ‘perfect asset’ to provide a match to the liability cash-flows and to provide the yield required to meet the aggressive premium target – with all parties monitoring the premium target daily on our monitoring software, Asset Liability Suite. The target was met in late June and the transaction completed within two working days.

For an insurer ‘close matched’ means the asset:

Whilst many pension schemes may take a similar approach, in reality most hedging strategies are designed to match the average duration and inflation sensitivity of the liabilities, and do not provide an exact cash-flow match. These differences may give rise to significant variation in outcome, for example where the interest rate curve changes shape or tilts, the insurer model should remain matched whilst the pension scheme approach gives rise to a mismatch. Furthermore, with the exception perhaps of the very biggest, most pension schemes don’t have the scale, expertise or appetite to negotiate bespoke terms on secure income, illiquid assets.

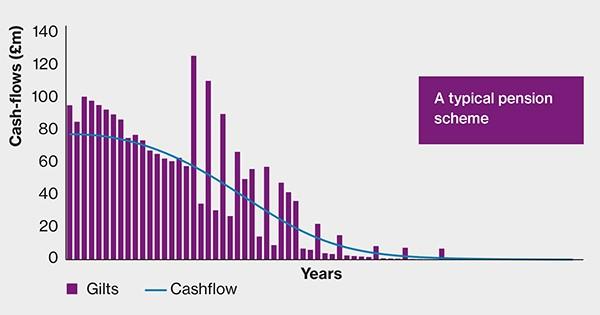

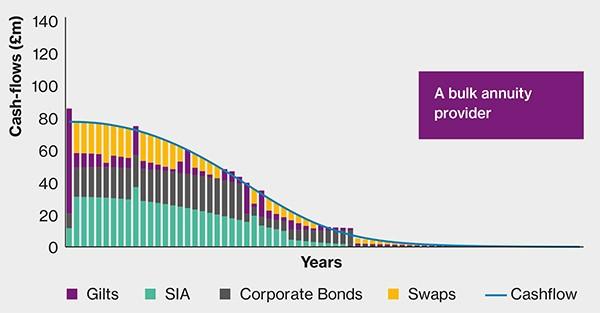

Figure 1 illustrates this difference. The first chart shows the pensioner cash-flows for a typical pension scheme, in this instance being backed by a portfolio of gilts. The second chart details the same cash-flows, but here the insurer has used a range of fixed income assets to achieve a greater degree of precision in the cash-flow matching.

The insurers’ approach is certainly working! Over the last six months we have seen extremely attractive pensioner buy-in pricing. We have helped our clients to complete over 20 buy-ins, achieving pricing relative to gilts that has not been available since the 2008 financial crisis.

| Title | File Type | File Size |

|---|---|---|

| Settlement in Focus July 2017 | 1.6 MB |