The Your Future Your Super (YFYS) legislative package was not primarily directed at insurance arrangements within super funds, but it will bring dramatic changes to new member flows starting on 1 November 2021, and significant long-term impacts for group insurance pricing and product design.

Employees who change jobs or careers after this date will no longer default to industry funds or corporate sub-plans, which have historically tailored insurance arrangements to the needs of the underlying occupation class and provided coverage directly linked to income levels.

Instead, disengaged employees will stay stapled to their first super fund, potentially from their first foray into the workforce as a teenager, without any recognition of changes in their salary or occupation. These members may be stapled to a fund with low cover, and few options to increase it to appropriate levels. This also increases the risk that the stapled fund may not provide optimal or competitive cover. Fund members who move into high risk occupations may find themselves without cover or options to increase it.

The YFYS stapling measure is the latest in a raft of legislative measures having a broad impact on group insurance and follows on from Protecting Your Super in 2019 and Putting Members Interests First in 2020 which saw a significant portion of inactive, young and low balance members, lose their cover.

Stapling will further fragment and dilute the historic group insurance pooling within super funds which has delivered insurance cheaply and efficiently to millions of Australians. Some of the broad impacts across the industry are likely to include:

higher insurance premiums arising from:

Consecutive failures under the YFYS performance test could be dire for insurance in affected funds as insurers could include this as a repricing trigger. The frozen membership may potentially be hit with increased insurance rates and result in the fund suddenly becoming unattractive to other potential insurers in a market tender.

Change of employment is typically a strong member engagement point. We expect some funds will leverage this to engage members and recalibrate insurance cover, so Life Events options may be expanded to include a change of employment trigger.

We may see the pricing of large employer-financed group insurance improve relative to broad based super funds where members pay for insurance. The ability to deliver a guaranteed 100% take up from a well-defined employee group allows certainty and better pricing.

The strong response from high risk occupation groups and their super funds has triggered a Treasury review into the appropriateness of occupational exclusions, and we expect this will result in a tightening or eradication of such exclusions for default cover.

Lastly, all funds will need to refocus on insurance premium cross subsidies by age as the insured membership profile of the whole industry is likely to change (and get older) over time. This will be a point of focus as the new entrant flow of young members may potentially be concentrated in a small number of funds, and the duplicate accounts of the younger cohort are consolidated.

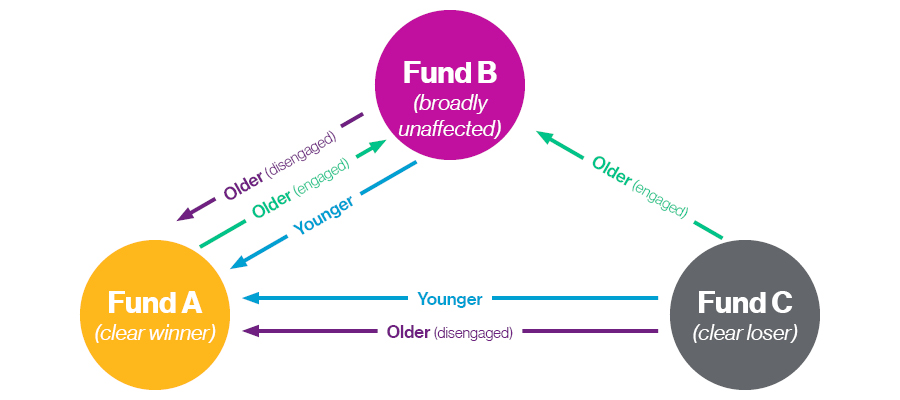

Our August 2021 article on YFYS impacts identified there will be clear winners and losers from the stapling reforms, through creating three example funds. We have extended this analysis to explore possible insurance implications:

Levels of member engagement are, to some extent, related to age, with members much more likely to increase engagement with their super as they get older. Therefore, we expect the increased member retention for Fund B to be an older rather than younger demographic. Net new entrant flows may therefore move according to Chart 1:

and how insurance design might respond, presenting an opportunity for funds to use insurance to attract and retain members.

and how insurance design might respond, presenting an opportunity for funds to use insurance to attract and retain members.

Clearly the goal for every fund is to avoid being Fund C. All funds will aspire to at least be broadly unaffected so let’s examine some of the insurance effects and possible actions from an insurance perspective for Fund A and Fund B.

Stapling will continue to increase the focus for funds on developing strong new entrant flows and engagement channels. In a performance test environment where being too different on investments may be a high-risk strategy, insurance design can play a key role in the attraction and retention of choice members.

However, funds also need to balance the additional risks that stapling may bring to their group insurance offering and consider the implications of long-term movements in underlying insured member demographics.