Lifetime income products in Australia’s superannuation sector represent a groundbreaking shift in retirement planning, offering members the ability to exchange a lump sum for a guaranteed income for life. However, pricing these products inherently relies on risk pooling – where the benefits for those who live longer are, in part, funded by those who die earlier. While this risk-sharing model helps super funds manage long-term obligations and is the fundamental basis of insurance, it does raise ethical concerns in price discrimination, particularly around the socio-economic factors influencing life expectancy.

Key drivers of life expectancy risk

When considering the drivers of life expectancy / mortality risk, there are a number of broad groups of driving factors. These categories can intersect and compound each other, adding complexity. For instance, lifestyle choices may be influenced by demographic factors, or environmental risks can be compounded by occupational exposure.

A question to consider is which of these risks should be pooled?

Perhaps a more nuanced question would be, in the context of lifetime income products, which of these risks should be pooled without commensurate adjustments to pricing for cohorts with different risk profiles?

In some countries, it is already prohibited to charge gender-specific annuity rates, while there has been increasing activity globally and within Australia regarding the use (or otherwise) of genetic screening results in the pricing of different insurance products.

Key drivers of life expectancy risk

Table 1: Key drivers of life expectancy risk

|

Category

|

Description

|

|

Genetic

|

Hereditary factors that influence health and predisposition to diseases, e.g., inherited disorders, genetic mutations.

|

|

Environmental

|

External factors related to physical surroundings, such as exposure to air pollution, toxins, or natural disasters. These can be driven by geographical factors, such as climate, urban or rural setting.

|

|

Demographic

|

Age and gender are the core drivers on which insurers have traditionally priced mortality risk.

|

|

Lifestyle and health

|

Personal habits and behaviours including pastimes, diet, physical activity, smoking and alcohol or drug consumption. This also includes mental health factors like stress, anxiety, and depression, which can impact physical health and mortality as well as pre-existing illnesses, e.g., diabetes, cardiovascular disease, that increase vulnerability to other health issues.

|

|

Socio-economic factors

|

Broad socio-economic status covering access to healthcare, education, employment, housing, and social support networks affecting overall wellbeing.

|

|

External forces

|

Exposure to pathogens and pandemics, with varying risk based on immunity, vaccination, and healthcare systems. Risks from injuries, accidents and violence, often linked to age, location, and occupation.

|

Contribution of socio-economic status to life expectancy

A core ethical issue lies in the fact that members from lower socio-economic backgrounds generally have shorter life expectancies, meaning they are less likely to fully benefit from lifetime income products compared to wealthier members. As such, these lifetime income products risk exacerbating existing inequalities, as those from disadvantaged backgrounds effectively subsidise the retirement incomes of those who are better off and likely to live longer. For trustees, this raises a critical question: how can they design lifetime income products that are fair and equitable and for which they can feel confident that they are discharging their fiduciary duties appropriately?

The paper “Life Tables by Relative Socio-Economic Advantage and Disadvantage” prepared by the Australian Government Actuary (AGA) for the Centre for Population, investigates the mortality experience of sub-groups of the Australian resident population based on relative socio-economic advantage and disadvantage.

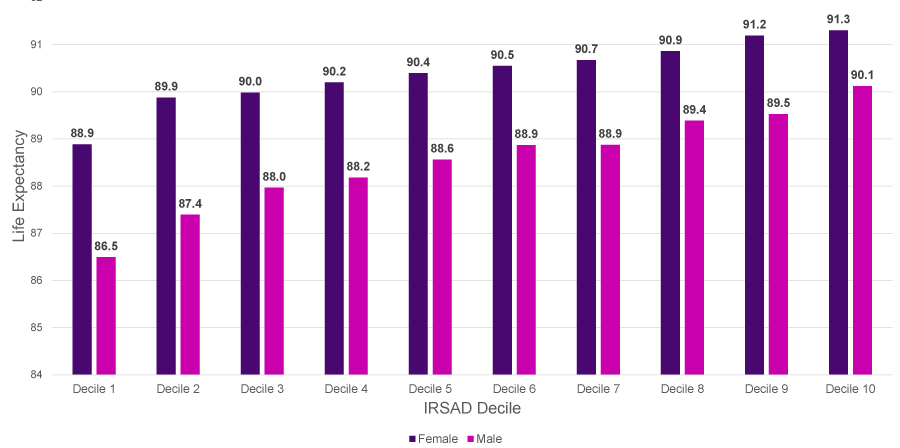

Distribution of life expectancy for 65 year olds (including 25 yr improvement factors)

Using the published mortality rates across the Index of Relative Socio-Economic Advantage and Disadvantage (IRSAD) deciles, and the 25 year improvement factors published by the AGA, we can see that there is quite a wide dispersion of life expectancies across from the lowest to highest decile of socio-economic status, with a 3.6 year difference for men and 2.4 year difference for women.

Balancing act

Australian superannuation trustees operate within a highly regulated environment where they must balance multiple obligations to ensure they meet their fiduciary duties. Key among these are the sole purpose test, the best financial interests duty (BFID) and the member outcomes covenant in the Superannuation Industry (Supervision) Act 1993 (SIS Act), expanded by APRA’s prudential standard SPS 515. Together, these obligations impose higher standards on trustees to focus on retirement outcomes for members and direct their energies towards member-centric activities to achieve them. They are now accountable for ensuring that all decisions are likely to lead to positive financial outcomes for members, encouraging a more rigorous assessment of costs, investments, and fund expenditures.

The sole purpose test focuses strictly on the provision of retirement, death or disability benefits. Historically this has constrained trustees from making decisions or investments that might provide broader benefits, e.g. wellness programs. The BFID and member outcomes obligations push trustees to optimise all aspects of fund performance and member experience, but the obligation to focus on financial outcomes means that non-core services or programs that enhance member engagement but may not be seen as directly relevant to retirement savings are increasingly difficult to justify.

But what if retirement benefits are linked to health and longevity? Does this give trustees scope to expand their remit within the boundaries of these obligations? Are they obliged to do so?

What can trustees do to manage these risks?

Distribution

One solution could be to ensure these products are targeted specifically at members most likely to benefit. Historically, annuity products have largely been acquired via advice arrangements where there is an inherent overlay of advisor judgement that would be expected to result in a more homogenous group of risk and life expectancy outcomes.

Trustees looking to build scale in these products through soft default arrangements need to carefully consider the appropriateness of these products for particular cohorts of their membership and whether this can reliably be accounted for in that soft default process.

Product Design

Another approach that trustees can take to mitigate the risks of inequitable treatment of member cohorts comes down to the design of the lifetime products.

For example, trustees could set minimum death benefit payments that aim to ensure that any members who pass away particularly early are given a fair and equitable “return” on their investment.

This would effectively delay the point at which mortality pooling begins to come into play, at which point the remaining cohort of lives might be a more homogenous group from a risk perspective. This is an approach we have seen adopted by some insurers offering annuity products in the market to date.

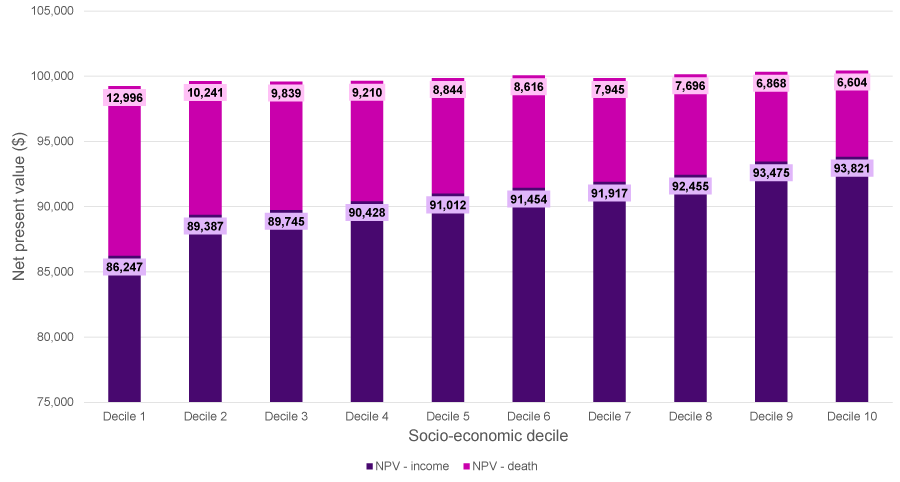

For example, the following chart illustrates the net present value (NPV) of future income and death benefit payments (assuming an initial purchase amount of $100,000) using the applicable mortality rates for each socio-economic decile based on an inflation-linked annuity currently offered by one of the providers in the market. As illustrated, the NPV ranges from 99.2% to 100.4% of the initial purchase price across the socio-economic deciles.

NPV – Inflation Linked Annuity

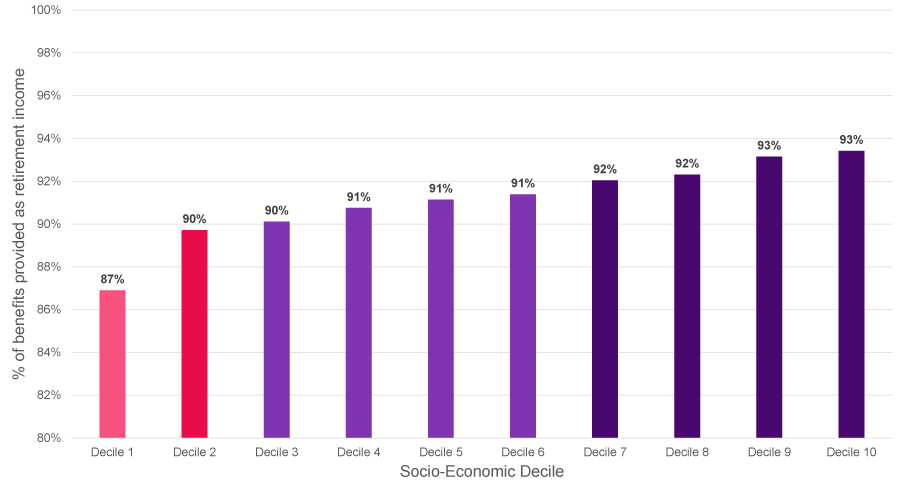

What does vary however, is the “income delivery ratio” or expected portion of benefits provided as retirement income rather than death benefits, with 87% of benefits being provided as retirement income payments for the lowest socio-economic decile compared to almost 93% for the highest decile. If the purpose of these products is to provide retirement income, then trustees will need to consider the disparity of outcomes in terms of type of benefit provided when designing or distributing such products.

Income Delivery Ratio – Inflation Linked Annuity

Pricing

While perhaps controversial, trustees could consider circumstances under which they might underwrite particular cohorts of members in order to identify their particular risk profiles and set pricing schedules that are tailored to these different cohorts. This is commonplace for death and disability insurance outside automatic cover provided under group policies, but it may ultimately prove to be too much of a barrier to entry in the lifetime income product space. Pricing different cohorts of members according to different risk profiles is also an area that may result in, or be seen to result in, discriminatory treatment of particular cohorts of members.

One obvious example of this would be gender specific pricing. This is commonplace in Australia for insurers selling annuity products, however other providers of innovative income streams have chosen to offer unisex income yields / pricing.

In some other countries, for example the UK, there are legislative restrictions on the use of gender as a risk factor by insurers when determining annuity income rates The question is when, not if, this will become a consideration or requirement here in Australia too. Indeed, in this regard we note the government’s intention to ban the use of genetic test results in life insurance underwriting.

Super HEALTH check?

When members live longer and healthier lives, they maximise the value of their lifetime income products, achieving more financial security. This linkage between financial outcomes and longevity arguably introduces an incentive for funds to look beyond investment outcomes and product solutions and consider services that enhance members’ health and quality of life as a means of delivering better member financial outcomes.

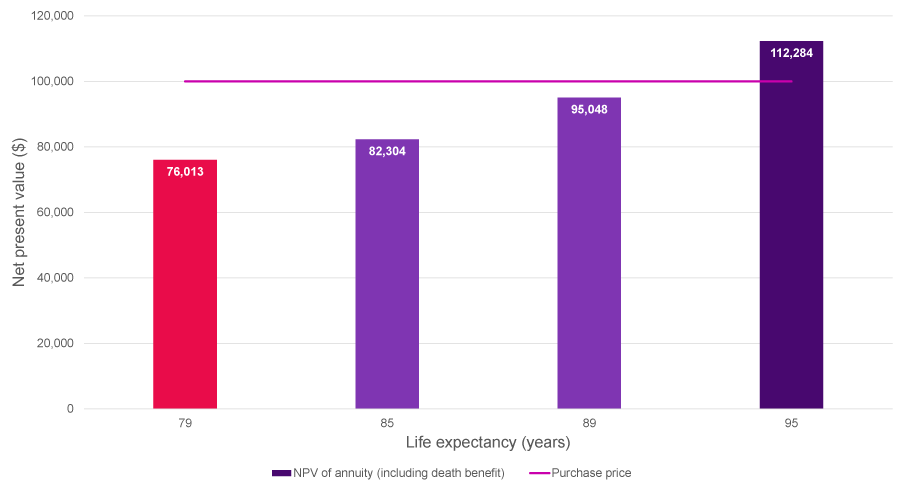

NPV of annuity compared to purchase price

With the rise of these products, super funds may be on the cusp of a dual responsibility—not only to invest wisely but also to actively support the health and longevity of their members. Carefully chosen and cost-effective services like health screenings, wellbeing programs or even partnerships with health providers, could potentially support members to live longer, healthier lives, maximising both their financial and physical/mental wellbeing in retirement.

A question that therefore emerges is, as superannuation funds increasingly offer lifetime income products, will trustees (and regulators) interpret their fiduciary duty to act in members’ best financial interests as extending beyond financial returns to also encompass the physical and mental wellbeing of their members? The answer could reshape the future of retirement in Australia, blending financial security with holistic wellness support.

Ultimately, trustees are faced with a balancing act: they must uphold their fiduciary duty to all members, while addressing the ethical pricing concerns associated with risk pooling and potential socio-economic inequities. By carefully considering member demographics, engaging in transparent communication, and exploring alternative structures, trustees can help ensure that lifetime income products are not only financially sustainable but also equitable and just for all members, regardless of background.

If you need help navigating anything Retirement related, reach out to WTW:

- Member Outcomes Assessment / Retirement Score Card

- Retirement preferences analysis

- Review of fund demographics and associated life expectancies to inform retirement product design

- Lifetime income product design, selection, pricing or solvency management

- Review of guidance and advice practices and tools to support the Retirement Income Covenant objectives and growing product suite.