Welcome to the latest edition of the Willis Natural Catastrophe Review, providing insight into recent significant catastrophe events and sharing expert views on the risks posed by major perils.

In this edition, we take a closer look at the major catastrophes that shaped the global conversation around risk in 2025, with emphasis on the second half of the year (Figure 1). Our analysis traces the chain of events behind each disaster, examining not only what happened but why. Beyond the immediate headlines, our team of experts digs into the structural pressures, overlooked warning signs, and systemic vulnerabilities that allowed these crises to take hold. We also share our perspective on the evolving landscape for catastrophic perils, offer advice to insurers seeking to update their view of these risks, and address the burgeoning affordability crisis in many markets.

Good luck is no substitute for sound strategy

Natural catastrophes caused more than $100 billion in insured losses in 2025, the sixth consecutive year above that threshold. But because losses were nearly $40 billion higher the year before, compared to recent experience, we might describe 2025 as a “moderate” loss year.

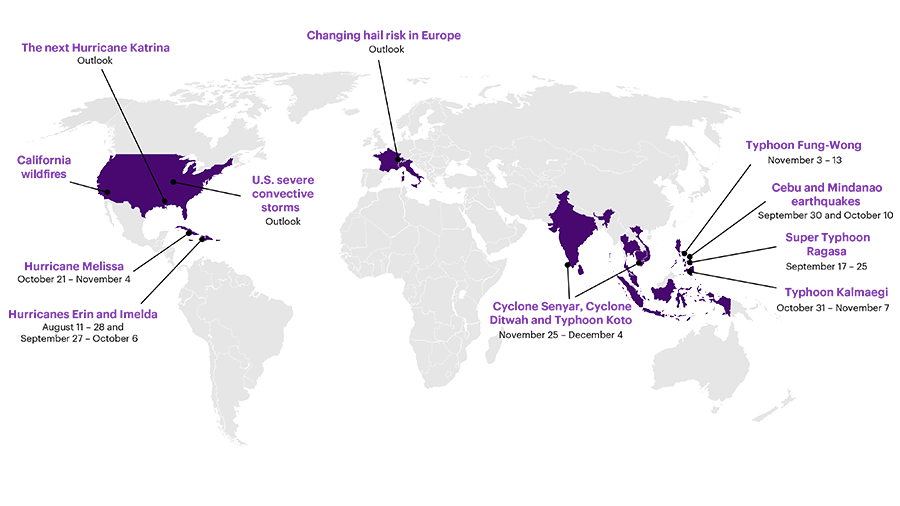

Figure 1: Map of key 2025 natural catastrophes covered in the report

However, losses above $100 billion – without even a single hurricane making landfall in the United States – should really regarded as evidence that catastrophe risks remain high. As Cameron Rye (Willis Re’s Director of Natural Catastrophe Analytics) points out in Section 2.1, the insurance industry should not allow the year-on-year decrease to lull it into a false sense of security. We know physical risks continue to increase as the world warms. And sooner or later, all lucky streaks end. Insurers should act now to protect their portfolios against unsustainable accumulations of risk and prepare for a reversal of fortune.

The shifting landscape of physical risks has also changed the responsibilities and roles of risk professionals. In Section 2.2, Torolf Hamm (Global Lead for WTW’s Physical Risks and Climate Practice) explains how risk managers can protect business value by working more closely with sustainability teams. By applying market-recognized approaches, risk functions can ensure physical risks are properly evaluated, make your organization more resilient to natural catastrophes, and embed risk awareness into organizational decision making.

Thanks to advances in catastrophe modeling, today insurers and reinsurers understand their true exposure to physical risks better than ever before. But while those improvements are necessary to price risk accurately, they do not address the growing affordability crisis facing the industry. Writing for the journal Nature (and reprinted in Section 2.3), Scott St. George (the Willis Research Network’s Head of Weather and Climate Risk) argues that insurers need to adopt new approaches to halt the upward spiral of risks and costs. Willis is a leader in this area – in April, Willis and the Nature Conservancy announced a first-of-its-kind wildfire policy in California that secured lower premiums and deductibles based on committed efforts to manage fuel loads in local forests.

A forward view on wildfire risk

For decades, wildfire experts have issued repeated warnings that prolonged drought enhanced by global warming and the continuing encroachment of communities into the wildland-urban interface would make catastrophic fires much more likely. Prior to 2025, there had been eight wildfires in California with insured losses greater than $2.8 billion (adjusted to 2024 US dollars), with 2018’s Camp Fire being the most destructive ($12.5 billion).

In January, we were confronted by the stark reality that wildfire can be much more severe. Together, the Eaton and Palisades Fires burned almost 60 square miles across Los Angeles County and destroyed more than 18,000 structures. According to the California Department of Insurance, as of this writing (January 14, 2026) insurers have already paid more than $22.4 billion to cover home, business, living expenses, auto damage, and other disaster-related claims related to the Eaton and Palisades Fires. Once all claims are paid, total insured losses for the Los Angeles wildfires may approach $40 billion.

The experience from Los Angeles provides unfortunate but undeniable proof that wildfire risk has increased substantially across California and the American west. And because claims from these events were so exceptionally high, going forward, wildfire must be considered a core contributor to the volatility of insurance portfolios. In section 3.1, Daniel Bannister (the Willis Research Network’s Weather & Climate Risks Research Lead) identifies the three main reasons why potential wildfire losses in California have gone up so dramatically during the past few years. And he reminds us that pricing cannot rely exclusively on historical losses – instead, we need to adjust wildfire models to present-day conditions, use detailed asset-level characteristics to supplement exposure data, and apply realistic estimates for replacement costs.

When trouble comes in company

When insurers and reinsurers attempt to gauge our exposure to losses arising from natural catastrophes, they usually examine each major peril in isolation. When we model the effects of major earthquakes, for example, we do not always consider what would happen if soils in the affected area were already saturated by heavy rainfall. And our scenarios often focus on one single catastrophic event, and either pay less attention or do not consider the (admittedly less likely) situation where the same place is affected by several perils in quick succession.

Unfortunately, we were reminded of the harm that can be done by multiple, compound perils, when the Philippines were affected by several major typhoons and earthquakes in short order. In Section 3.2, James Dalziel (the Willis Research Network’s Earth Risk Research Lead) describes the cumulative damage wrought by Super Typhoon Ragasa, four large magnitude earthquakes and aftershocks, and two other landfalling typhoons. As noted in his commentary, this sort of complex, multi-hazard sequence can often lead to delayed claims payments and disagreements with policy holders. They also create opportunities for disaster risk financing products specifically tailored to reduce the economic impact of a similar sequence of catastrophic events.

Is a hot North Atlantic causing hurricanes to level up?

Heading into the 2025 North Atlantic hurricane season, forecasters were calling for an above-average number of storms but assigned a wider range to their predictions than they did the year prior. The consensus view was that high ocean temperatures in the North Atlantic would be counterbalanced by neutral conditions in the central Pacific, and so the upcoming season would be quite active but not as stormy as 2024.

As things turned out, forecasters were correct about the number of named tropical storms (13, low but well within the forecast range) and the number of major (Category 4 or 5) hurricanes (four storms, which was the most common prediction). By contrast, it was a clear miss for the number of hurricanes. Only five North Atlantic storms reached hurricane status, and no forecasting center predicted such a low number (predictions ranged from six to 10, with seven, eight, or nine hurricanes being the most common forecast).

Is the near absence of “moderate” hurricanes (storms that reach Category 1, 2 or 3) this year the result of random chance or is it a sign of changing storm behavior? In Section 3.3, Willis Research Network Senior Fellow Dr. James Done (National Center for Atmospheric Research) lays out a possible physical explanation for the apparent ‘disappearance’ of weaker hurricanes. As he explains, it used to be that large expanses of the North Atlantic remained (relatively) cool during the hurricane season, and so those parts of the ocean could only support moderate- strength storms. But today the North Atlantic is consistently hotter everywhere, so more of the surface ocean has sufficient energy to give rise to the strongest hurricanes.

2025 was the first year in a decade where no hurricanes made landfall in the United States, but other places were not so fortunate. Hurricane Erin followed an eastward track well away from the Caribbean but still delivered heavy rain to Guadeloupe and Puerto Rico and high winds to the Bahamas. Hurricane Imelda passed directly over the northern coast of the Dominican Republic and Haiti and brought heavy rains and severe flooding to both countries. The storm also caused heavy rain and landslides in Cuba and strong winds (with gusts up to 100 miles per hour) over Bermuda.

The most consequential event of the past season was Hurricane Melissa, which made landfall over Jamaica on October 28 as a Category 5 storm. In Section 3.4, Toby Jones (Catastrophe Research Analyst in the Willis Research Network) explains why this region may see more storms like Melissa in the future. It was previously uncommon for major hurricanes to form in October, but as the North Atlantic has warmed, the environmental conditions that are favorable to hurricane formation are lasting later in the year. And that same warming also allows storms to become much stronger very quickly – compared to the late 20th century, the number of storms undergoing “explosive” intensification (winds strengthening by almost 60 miles per hour in less than a day) has almost doubled.

Heavy rains overwhelm capacity in many places

As the world continues to warm, we expect both ends of the hydrological spectrum – flood and drought – to become more intense. The second half of 2025 featured extreme or record-setting rainfall in many locations, leading to numerous cases of severe flooding in places not typically considered to be high risk.

In Section 3.5, Professor Hayley Fowler (Newcastle University) and Neil Gunn (Head of Flood and Water Management Research at the Willis Research Network) explain why it’s so important to understand that flood risk is not confined to formally defined flood zones. They draw particular attention to the risk posed by pluvial flooding, which occurs when intense rainfall overwhelms surface drainage and causes high water in places far removed from rivers, lakes, or coasts. Because flood maps provided by the public sector often do not account for pluvial flooding, risk managers ought to think broadly about their exposure to all types of high water and adjust their insurance coverage accordingly.

Over the course of a single week, several parts of southeast Asia were affected by heavy rains and widespread flooding triggered by three typhoons in rapid succession. In Section 3.6, Srivatsan Vijayaraghavan (National University of Singapore) and Daniel Bannister describe the unusual background conditions that gave rise to Cyclone Senyar, Cyclone Ditwah and Typhoon Koto, allowing them to rapidly intensify and produce exceptionally high amounts of rain. They also use a simulation exercise supported by the Willis Research Network to consider how tropical storms in the western Pacific will respond to future warming. According to those experiments, in a warmer world, we should expect Pacific typhoons to have higher winds, exhibit deeper convection, and produce more intense rainfall.

All signs point to increasing storm risks

Traditionally, the insurance industry has classified tornadoes, hail and other aspects of severe convective storms as ‘secondary’ perils. That meant they accounted for a relatively small share of total losses from catastrophes and did not have the same potential as hurricanes or earthquakes to produce extremely high losses. But over the past several years, total claims from severe convective storms have increased substantially, matching or even exceeding in some cases the total losses from ‘primary’ perils.

Have we experienced a run of bad luck with respect to severe weather (particularly in the United States)? Or has the risk landscape changed so much that the industry ought to plan for continued high losses from this peril? In section 4.1, Scott St. George puts those questions to two leading experts. In that conversation, Kelsey Malloy (University of Delaware) explains how the physical environment that gives rise to severe weather today compares to previous decades and how those factors will continue to evolve over the next few years. And Cameron Rye shares his thoughts on the social and economic factors that have caused the sudden up-step in loss potential from severe storms.

In Europe, the exposure to severe weather is not as high as in the United States, but there are reasons to worry those risks are going up. In Section 4.2, our partners at the Karlsruhe Institute of Technology, Jannick Fischer and Michael Kunz, along with Willis’s Daniel Bannister, provide their expert view on how hail is changing in Europe. First, although no single metric can adequately represent all aspects of hail risk, the general state of the atmosphere across Italy, Switzerland, Austria, and southern France has become more favorable for large hail. Second, simulations using high-resolution models predict that future hailstorms will, on average, generate larger hailstones. Third, we expect to see the greatest increase in hail risk for those places that are already hail ‘hotspots’ (specifically Austria, Italy and parts of Switzerland).

Envisioning the next Katrina-scale catastrophe

Twenty years have passed since Hurricane Katrina redefined the insurance industry’s upper bound for losses from a single catastrophic event. In terms of insured losses, Katrina is not only the costliest natural catastrophe on record but also exceeds the second-place event (2022’s Hurricane Ian) by a factor of nearly two.

The unprecedented cost of Katrina certainly has prompted insurers and reinsurers to change the way they do business. Today, the industry has learned to better diversify risk by geography, consider potential infrastructure failure as part of hazard modeling, and adjust loss estimates upwards to account for higher rebuilding costs following catastrophic events. But it also almost guaranteed the next “Katrina-scale” catastrophe will not simply be a repeat of the event itself.

In our final article (Section 4.3), Jessica Boyd (the Willis Research Network’s Head of Model Research) and Daniel Bannister challenge the industry to think through the consequences of an entirely new sort of major catastrophe. As they point out, too often we base our view of risk on the most recent event within our experience. We would be better served by considering a broader set of possibilities. Those possibilities could include past events adjusted in realistic ways (for instance, what if 2022’s Hurricane Milton had made landfall closer to Tampa Bay, as originally forecast?) or historic events applied to present-day exposures (what would be the insured loss if a repeat of the Great Miami Hurricane of 1926 happened today?). Instead of planning for the last record-setting catastrophe, the industry ought to use its imagination to prepare for an event that will be just as much as surprise as Katrina was in 2005.