Pension levelling options are not new. However, with many schemes providing an ever-increasing range of flexibilities to members, Edd Collins explores the benefits of offering such an option for both members and sponsors of defined benefit (DB) schemes.

A pension levelling option allows a member to reshape their scheme pension to better integrate with the State Pension, such that they receive a level total income throughout retirement, is something that many schemes have always had in place. However, they have often been poorly advertised and consequently seldom used.

That said, there has been renewed interest in these options recently. With the State Pension age (SPA) due to increase beyond 65 for the first time in 2018, the attractiveness of such options has increased from a member’s perspective. At the same time, persistent deficits are forcing employers to continuously look for opportunities they can take to help them better manage their pension liabilities. Pension levelling options can therefore present a win-win for both the employer and the pension scheme member.

What is a pension levelling option?

A pension levelling option is available to a member retiring before SPA that allows them to bring forward the payment of part of their scheme pension, such that they will not see a step-up in their overall retirement income at SPA. The member thus has the option to receive a level pension income throughout their retirement (their pension would still be subject to any inflationary pension increases in the usual way, but they would not see any large increases in their income during retirement).

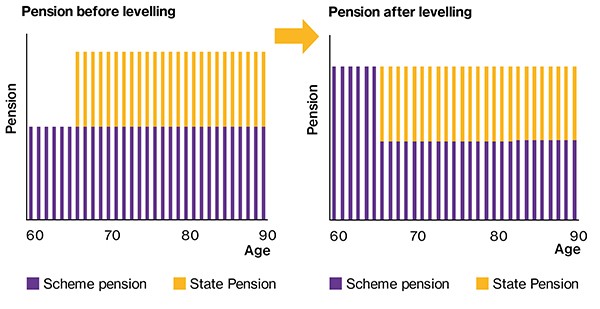

The charts below illustrate the effect on a member’s retirement income from taking such an option (ignoring future increases for simplicity).

Figure 1. Example of pension levelling

What does this mean in practice for a member? Well, if they were expecting to retire at age 60 with a pension of £10,000 a year and choosing to take their maximum tax-free cash lump sum of just over £66,000, Figure 2 shows that a typical scheme member could instead receive a pension and tax-free lump sum at age 60 that are each over 50% higher if they were to choose a level pension option.

Figure 2. Impact on typical scheme member benefits

| Pre-levelling option | Post-levelling option | Impact | |

|---|---|---|---|

| Pension from 60 | £10,000 | £15,300 | 55% increase |

| Tax-free cash | £66,700 | £101,700 | 55% increase |

| Pension from 66 | £18,300 | £15,300 | 15% reduction |

| Funding liability | ~£435,000 | ~£410,000 | 5% reduction |

At the same time, you can see that the employer would also see a reduction in their pension liabilities for this member of around 5%.

Why are employers interested in offering pension levelling options?

Clearly, the liability reduction noted above is a key driver for employers pursuing pension levelling options. However, there are a number of other potential benefits:

- Risk reduction – benefit payments paid further into the future are more uncertain and so create greater risk for the company. Reducing these later benefit payments reduces the overall risk level.

- Workforce planning – providing members with a higher initial pension may enable early retirement for a greater proportion of members, which may help with workforce planning.

- Bringing forward cost savings – if the option results in more early retirements, this will accelerate likely cash commutation savings.

Why are members interested in taking pension levelling options?

The table above highlights the potential impact on a member’s pension. This will be attractive to many members for a number of reasons:

- Greater retirement flexibility, particularly for lower earners – by allowing members to access more of their benefits before SPA, this option may enable early retirement for more members than would otherwise be the case. Some members may find this even more attractive as SPA begins to increase beyond age 65.

- Greater flexibility over the shape of retirement income – a number of members may have a preference to access their benefits earlier in retirement, to better meet their expected outgo and so that they can spend their money at a time when they may feel best placed to enjoy it. A pension levelling option may allow them to receive both a higher initial pension and a higher tax-free lump sum.

- Avoids an unnecessary step-up in retirement income – for many members, seeing a step-up in their retirement income when they reach SPA is unnecessary. Therefore, they may believe it is easier for them to plan their retirement if they opt for a level pension, which does not result in a large step-up during retirement.

What do I need to think about before introducing such an option?

As with any option being presented to members, it is important that members are provided with all the necessary information to make an informed decision. Clear communication of the option will therefore be key, although this can be incorporated as part of existing communication on their other retirement options.

For members, particularly higher earners, there will also be a need to consider potential tax consequences related to their annual and lifetime allowances that may arise from seeing an increase in their initial retirement pension.

Is it possible to go further?

Although we have referred to this option as pension levelling, the legislation surrounding such options does enable schemes to go further. At the extreme, a member could choose to reshape their pension such that they have a reduction in their scheme pension equal to two times the new flat rate State Pension at SPA. This effectively enables a step down at SPA of around £16,000 a year.

Extending the option this way could provide DB members with even greater flexibility as to how they take their pension, bridging the gap between the flexibility available to DB and DC members, and further increase the cost and risk savings for employers.