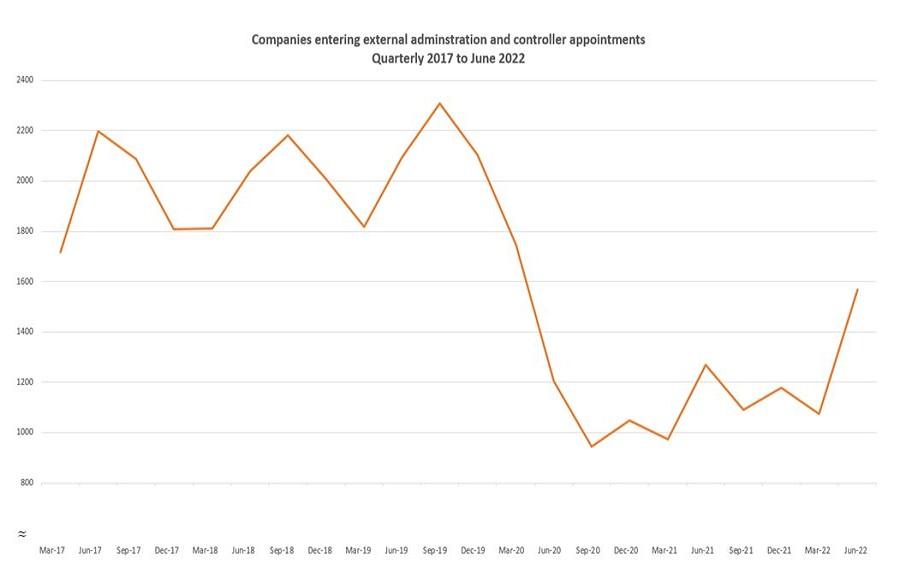

Insolvency filings are increasing across Australia. In the 2022 financial year, there were 6,555 external administration and controller appointments, a 7.9% increase over 2021. Hospitality, retail and construction were sectors of particular concern, increasing 28.4%, 34.7% and 26.1% respectively in the past year.

While safe harbour provisions gave Australian directors and executives protection over insolvent trading during the COVID-19 pandemic, these have ended, as have government assistance programs relied upon to mitigate cash management issues and reduced business inflows. Combined with rising inflation and the prevalence of fixed cost contracts, pressures across a range of organisations continue to mount and Australia has already seen several high-profile collapses. So, for organisations facing insolvency, will Directors’ and Officers’ (D&O) cover now provide the last line of defence?

Although the appointment of external administrators is increasing, numbers are still far below pre-COVID levels. However, the challenges for Australian companies finding themselves in trouble are manifold. Where corporate indemnification protections are limited, D&O coverage may be the only defence to which directors and executives can turn.

Source: ASIC1

As insolvencies continue to increase, understanding the coverage available under a D&O policy will assist risk professionals during internal conversations with their boards and executives. Close focus is particularly needed when D&O programs are due for renewal, ensuring coverage remains as broad as possible, limit adequacy modelled and considered to meet risk strategy requirements and any restrictions negotiated.

Broad coverage for insolvency-related claims is generally contemplated within the D&O policy. Direct or derivative claims may be filed by creditors and/or administrators who may allege breaches of fiduciary duty, corporate waste and/or deepening the insolvency.

In those cases, defence costs, compensatory damages, and settlements are generally subject to coverage; however, other policy provisions may be relevant, depending on the scope and nature of any given matter. Those may include:

D&O insurance is a policy designed to cover third party liability exposures. Nevertheless, the policy often includes first party coverages that could be beneficial to companies that are insolvent or in the zone of insolvency.

First party coverage may be available in certain instances for crisis management expenses to the extent a company has experienced a “crisis”, as defined in the policy. Events that may trigger coverage include negative earnings announcements, key executive resignations, employee layoffs, product recalls, and elimination or suspension of dividends, among others. The coverage is customarily subject to a sub-limit of liability.

Similar to crisis management coverage, some policies may include first party coverage for a director’s or officer’s “reputation crisis”. Also, traditionally sub-limited, the coverage may be applicable to individuals to the extent their reputations are adversely impacted in crisis events. The triggers may be narrow and could require the act of an enforcement authority.

Understanding what your D&O policy offers and making informed decisions at executive and board level is crucial ahead of any renewal process. WTW’s expert Financial, Executive and Professional Risks (FINEX) team and dedicated insolvency practice can help evaluate your organisation’s cover, design appropriate risk mitigation and transfer solutions and secure the best possible terms.

1 https://asic.gov.au/regulatory-resources/find-a-document/statistics/insolvency-statistics/insolvency-statistics-series-1-companies-entering-external-administration-and-controller-appointments/?mc_cid=b371648ebc&mc_eid=95f16a64b1