Key global HR, benefits and pay takeaways to watch in 2024

Multinational organizations understandably prefer uniform, global policies. After all, this makes everything more efficient and consistent, and lends “relative” ease to doing business on a large scale. However, an increasingly complex world often is at odds with a global, one-size-fits-all approach, especially as of late.

The International Monetary Funds (IMF’s) October 2023 World Economic Outlook report points to the issue of “increasing geoeconomic fragmentation,” where states are increasingly willing to take unilateral actions to pursue their economic and geopolitical interests, thwarting decades-old regional and global integration trends. Concurrently, many economies have emerged from the turbulence of 2020 through 2022 keen to relaunch reform programs that previously were put on hold, even as fears around inflation, growth and regional conflicts persist and exert pressures of their own.

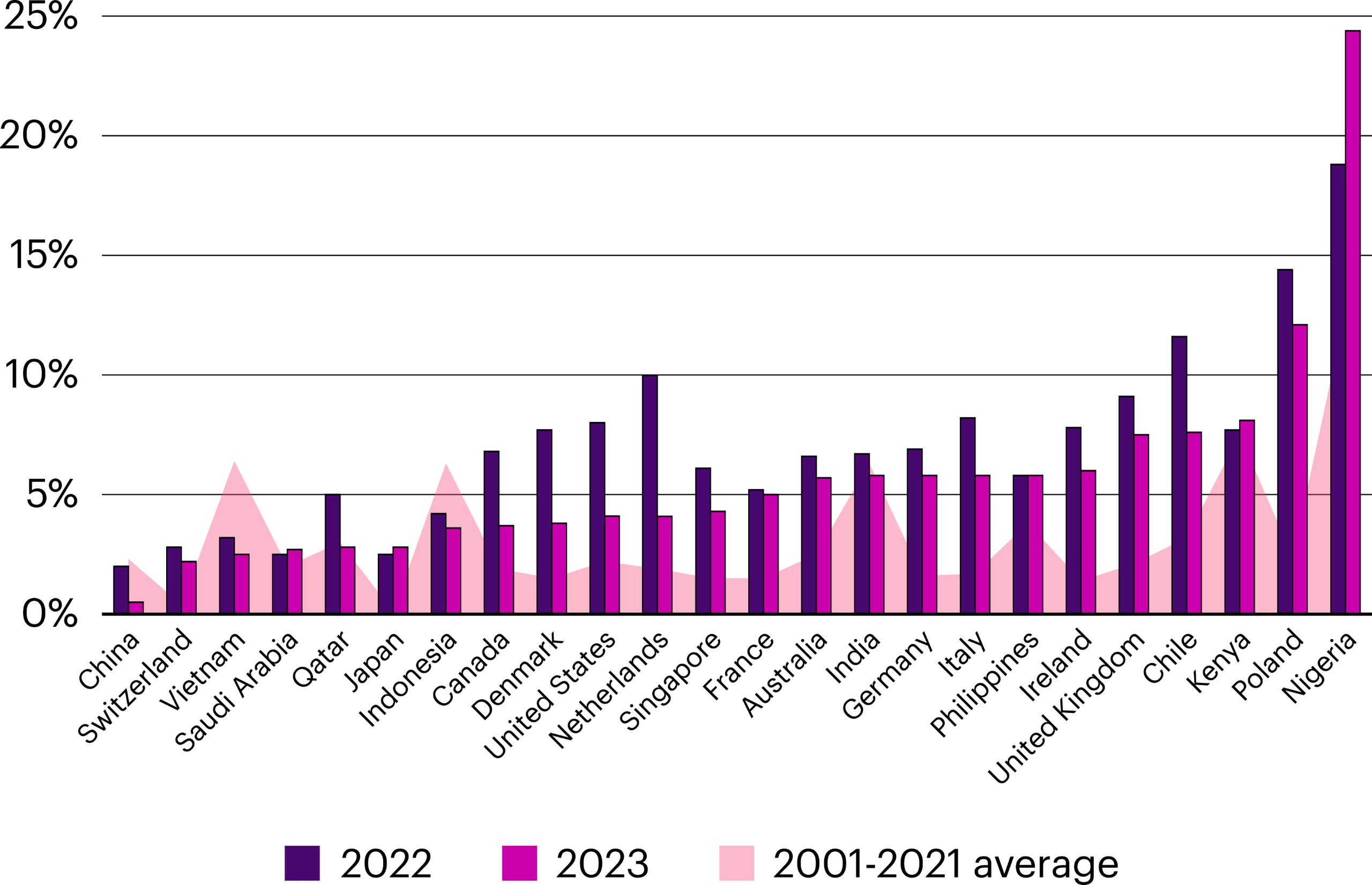

Since the latter half of 2022, high inflation rates in many countries have commanded a great deal of attention, and governments, employers and workforces have reacted in a variety of ways. While 2023 inflation projections are mostly lower than 2022 levels (substantially lower in some cases), rates still are above pre-pandemic “normal” inflation rates in most places. At the same time, with a few notable exceptions (like the U.S.), post-pandemic economic activity has generally been weak. The IMF expects a 2.9% global growth rate in 2024, well below an annual average of 3.8% in the two decades prior.

Long story short: Today’s global business environment is characterized by less economic integration, slowing growth and a lot of uncertainty in general (see Figure 1).

Source: International Monetary Fund World Economic Outlook Report, October 2023; Oxford Economics

After several years of employers’ attention being dominated by singular, historic events that imposed an unusual sense of urgency, employment environments are exhibiting a more characteristic patchwork of short- and long-term pressures, influences and opportunities. However, this is not to say that organizations are “returning” to anything in particular, be it the pre-pandemic status quo or previously interrupted reforms.

Despite a gradual slowdown in economic activity, employment has not followed suit. At the beginning of 2023, the International Labor Organization’s (ILO) World Employment and Social Outlook report predicted that the economic slowdown was “likely to force workers to accept lower quality jobs.” Ten months later, the UN’s World Economic Situation and Prospects October Briefing observed that “labor market conditions in most developed economies remain robust in 2023.”

As a result, rather than shed staff to reduce costs, many employers responded to protracted cost-of-living pressures by providing higher than normal pay increases or one-off lump-sum payments (while seeking to offset increased – and often unbudgeted – compensation costs in other ways). Employers also had to contend with external pressures such as legislative changes, new employer mandates or more aggressive collective bargaining by unions (where they exist). Higher employment costs are the result in all of these scenarios.

Where those cost increases weigh most heavily varies greatly of course. In comparatively expensive markets, such increases can wreak havoc on budgets when headcount remains stable or increases, creating cost pressures that may need to be actively addressed. Conversely, “expensive” markets often tend to be relatively more developed and lucrative (for operations in which most staff are profit center-based as opposed to cost centers). Thus, employment cost changes – whether due to increased compensation higher employer benefit contributions or costlier benefit entitlements – should be viewed in the context of the market concerned.

Take, for example, median total guaranteed compensation (TGC) levels for graduates and administrators (broadly represented by WTW survey grade 8). Across the 64 markets covered by the 2023/2024 Global 50 Remuneration Planning Report, median rates vary greatly, with the highest paid market being more than 15 times greater than the lowest paid (see Figure 2). As such, increases in employment costs will affect regional and global budgets quite differently. In addition, for companies looking for cost-attractive locations related to functions that are considered “mobile,” there is a wide range of options (availability of talent, among other things).

While these pressures, influences and opportunities are constantly jockeying for attention, it’s easy to forget that there are a whole host of other concerns employers must address.

According to the Global 50 report, which highlights more than 180 key developments in compensation, benefits and employment across 64 markets, retirement and paid leave entitlements are the most commonly affected areas among the developments covered in the report, globally (see Figure 3).

Certain trends also can be observed regionally. The most noteworthy example is Europe: All 27 EU member states were required to transpose EU directives on work-life balance and employment transparency into local laws. The impact on national labor laws stemming from transposition varied, with the most noteworthy changes being to family leave entitlements, including short-term situational leaves, and the right of employees to request more flexible work (e.g., part time, flexible hours, remote/hybrid working) or more predictable work schedules.

Most of these changes took place in 2023 and, as a result, Europe accounted for more change than any other region, with Western Europe in particular representing almost 40% of all reported developments. At the opposite end of the scale, the Middle East and Africa represented less than 10% (see Figure 4).

While governments were busy in the areas of compensation, benefits and labor laws in 2023, there is little reason to believe the pace will slow this year. Among all of the developments reported in the Global 50 report, more than one-third were not in full effect as of Nov. 1, 2023, including several reforms that are being rolled out over a multi-year period (see Figure 5).

With more regulatory changes on the horizon and no “going back” to any former state, it is important for employers to stay abreast of all of the factors that influence their approach to compensation and benefits programs and policies. Consistent, reliable and timely data is the first tool all HR professionals should add to their kit as they address the challenges that will invariably come.