While disaster risk frameworks have traditionally focused on property damage and direct economic losses, population displacement is emerging as a critical risk multiplier.

Understanding disaster-induced displacement risks

Displacement is one of the most direct expressions of human vulnerability; it captures the point at which environmental and social systems fail to protect people, forcing movement as the last form of adaptation. According to the 2025 Global Report on Internal Displacement, disasters triggered a record-high 45.8 million displacements in 2024, with population growth in hazard-prone areas and climate change likely to increase risks in the years to come. The challenge is global: The reported displacements spanned 163 countries and territories, with the United States (11 million), the Philippines (9 million), India (5 million), China (4 million) and Bangladesh (2 million) accounting for the most significant shares.

45.8m

displacements due to disasters in 2024 - a record-high

Not all displacements are equal. Over 8 million of the recorded displacements were preemptive evacuations — a form of disaster displacement that can save lives and is usually short term. For example, roughly twothirds of households displaced due to disasters in the U.S. reported returning within a month, according to the Household Pulse Survey. Meanwhile, households that are unable to return quickly often face immense hardships, including job loss and income decline, disrupted education, increased post-traumatic stress and other psychosocial effects.

Figure 1: The number of disaster-induced displacements reported globally between 2015 and 2024

Protracted displacement also undermines broader economic recovery. Communities face substantial economic production losses when residents cannot return home to resume their daily activities. For example, according to the Internal Displacement Monitoring Centre, a loss equivalent to 2% of Nepal’s GDP is attributed to the economic production lost from displacement after the 2015 Gorkha earthquake. In contrast, only 0.01% of Mexico’s GDP is attributed to lost economic production from displacement after the 2017 Puebla earthquake, in part because residents were 15 times less likely to be displaced and returned home twice as quickly. Insurance penetration can also stimulate spending in local economies after a disaster. For example, one study has shown how a 10% increase in flood insurance take-up rate leads to 15% more visits to local businesses at a given depth of flooding after hurricanes in the U.S.

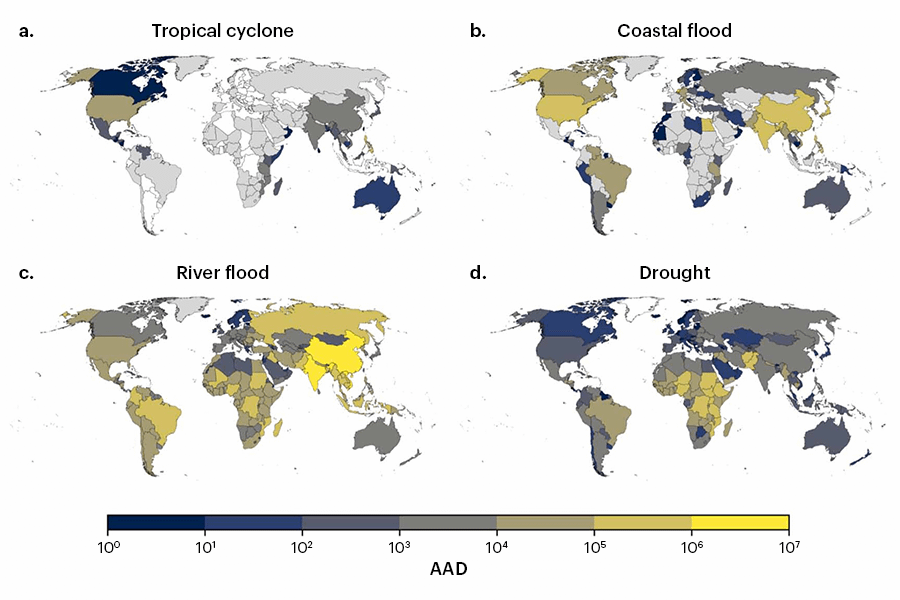

Recent modeling advances are beginning to capture the human and societal consequences of disasters, including displacement. For example, Meiler et al. (2025) adapt the disaster risk framework commonly underpinning (re)insurance models to quantify global displacement risks for tropical cyclones, coastal floods, river floods and droughts for both present-day and future climate scenarios. Ongoing work funded by the Willis Research Network and the Internal Displacement Monitoring Centre will similarly extend the disaster risk modeling framework to estimate earthquake-triggered population displacement globally, in collaboration with researchers at University College London and the Global Earthquake Model Foundation.

Figure 2. Average annual number of people displaced due to (a) tropical cyclones, (b) coastal floods, (c) river floods and (d) droughts (Meiler et al. 2025)

Research has made progress on capturing displacement duration in the U.S.: Paul et al. (2025) fit machine learning models to data from nearly 12,000 disaster-displaced American households to predict whether a household will return within a month, beyond one month or potentially not at all. The study demonstrates how higher levels of property damage are associated with the most adverse consequences, including displacement lasting beyond one month and no return. However, notable secondary drivers include socioeconomic factors such as the household’s tenure status and income level.

Managing growing humanitarian costs

Despite contributing the least to human-induced global climate change, people residing in low and lower-middle-income countries are the most vulnerable to its worst effects. The International Federation of Red Cross and Red Crescent Societies (IFRC) projects that the number of people requiring humanitarian assistance due to climate-related disasters could double from 108 million in 2019 to 200 million annually by 2050. Yet, the humanitarian system is already under strain, with emergency shelter being one of the least-funded sectors, having received only 28% of the required amount worldwide in 2024. How can we sustainably finance these growing risks, especially for the most vulnerable populations who lack formal insurance coverage?

One promising development is the use of an insurance mechanism to strengthen the IFRC’s Disaster Response Emergency Fund (IFRC-DREF). The IFRC-DREF is a central donor-funded pot of money that has rapidly released to local Red Cross and Red Crescent societies for early action and immediate disaster response since 1979. In 2023, IFRC partnered with Aon to design an indemnity insurance policy that protects the DREF itself. Rather than covering individual disasters, the policy triggers when aggregate allocations surpass a threshold. Donors now have the option to pay the insurance premium, rather than funding disaster responses as a traditional grant, transferring risks to the private sector when IFRC-DREF funding requests exceed available resources. Super Typhoon Yagi in Asia triggered the first payout in 2024, marking the first time a single, worldwide commercial indemnity insurance policy covered the emergency humanitarian costs of a disaster. This mechanism creates more predictable budgeting and ensures additional funding capacity during years of unexpected volatility, illustrating how insurance can help maintain global safety nets that safeguard the most vulnerable.

Other insurance mechanisms exist to help the most vulnerable countries manage the increasing costs of disasters. Globally, the Vulnerable Twenty (V20) Group partnered with the Group of Seven (G7) to launch the Global Shield Against Climate Risks in November 2022, aiming to strengthen the financial protection and resilience of vulnerable countries and people by increasing access to prearranged finance. Regional risk pools have also formed. The Caribbean Catastrophe Risk Insurance Facility (CCRIF), established in 2007, was the world’s first multi-country, multi-peril risk pool based on parametric insurance. It now has 30 members across the Caribbean and Central America, providing rapid payouts for tropical cyclones, excessive rainfall and earthquakes. Similar regional risk pools have since been developed in Africa and the Pacific.

Reimagining the role of insurers to reduce future risks

Financing response is only part of the challenge and reducing future risks requires tackling key drivers of increasing displacement risks. Evidence consistently shows that property damage is the strongest determinant of long-term displacement. One of the most effective strategies to reduce displacement risks would be to prevent homes from becoming uninhabitable in the first place. Once homes are destroyed or rendered uninhabitable, households face the most prolonged, difficult and expensive recovery trajectories.

Insurance for Good, a nonprofit and community of practice, is reimagining how insurers can drive systemic resilience rather than merely transferring risks. They have proposed two mechanisms that could leverage the post-disaster reconstruction period as an opportunity to build more disaster-resistant communities, thereby reducing future risks. These proposed tools not only would benefit households and communities but could also help stabilize insurance risks in the longer term.

The first proposed solution is climate-ready rebuilding endorsements, which are add-ons to standard insurance policies that provide extra coverage for specific upgrades. When households face substantial damage to their home, they often interface with insurers to finance reconstruction and make decisions on how to rebuild. Integrating upgrades during rebuilding is typically more cost-effective than undertaking retrofits; however, homeowners may lack the necessary information about what actions to take or be unwilling to absorb any increased costs after a disaster. Insurers are uniquely positioned to provide advisory support and adapt claims to support additional payments for resilient or green home improvements. For example, the State of Alabama requires insurers to offer FORTIFIED Roof™ endorsements as an add-on option to policyholders. These roofs protect against wind and wind-driven rain by improving the roof sheathing attachment, providing a sealed roof deck and reducing the likelihood of attic ventilation system failure at an additional cost estimated between $700 and $1,700.

A second proposed solution addresses high-risk areas, such as coastlines threatened by sea level rise or regions facing recurrent wildfires. Rebuilding may not be sustainable in these areas, and insurance policies could adapt coverage to support relocation costs more flexibly when a household deems future risks untenable. Ideally, these mechanisms would be paired with a home buyout program to prevent new tenants from moving in and perpetuating risks.

Beyond damaging assets and incurring direct economic losses, disasters can trigger largescale displacement. These displacements include preemptive evacuations that can save lives and be short term, but not all households can quickly return after a disaster. Protracted displacement disrupts lives and can create ripple effects that stall economies. Disaster risk modeling frameworks, such as those used in the (re)insurance sector to quantify property damage and economic loss, are now being extended to capture population displacement. Additionally, innovative insurance mechanisms are now being explored to protect the most vulnerable and to incentivize safer (and greener) rebuilding. The challenge ahead is to refine these tools and scale these approaches to transition from reactive disaster response to anticipatory action and long-term risk reduction, thereby building more equitable community resilience.