The Indian semiconductor industry was import-driven, primarily importing from countries including China, Taiwan, USA and Japan. The vision of India’s Atma Nirbhar (self-reliance) in electronics and semiconductors market gained momentum with the Indian Government’s approval of INR 76,000 Crores for the development of semiconductor and display manufacturing in India.

With growing markets, not just for automobiles but for smart wearables, mobile phones etc., the demand for semiconductors is at an all-time peak.

Emerging trends in the industry

- Skilled workforce and cost-effective solutions: India has a large pool of engineering and technical talent, and the availability of highly educated and trained workforce has been a key factor in attracting semiconductor companies to India. In fact, the semiconductor market is projected to generate employment for 600,000 people by 2030.

- Role of Government policies: India has established itself as a globally competitive hub of Electronics System Design and Manufacturing (ESDM) through initiatives like “Make in India” and “Digital India”. The National Policy on Electronics (NPE) aims to boost domestic manufacturing, attract investments, encourage innovation and create a conducive ecosystem for the electronics sector.

- Growth and development: With the rapid growth of the Indian economy and the increasing adoption of electronic devices, the demand for semiconductors is also growing. India’s semiconductor market is expected to reach USD 64 billion by 2026, as compared to its last valuation of USD 22.7 billion in 2019.

- Strategic importance: The Indian Government aims to reduce its dependency on imported semiconductors and instead aims to build indigenous capabilities within the country.

Challenges faced by the industry

- Supply chain challenges: Ensuring smooth operations at each stage is essential to avoid any shortages and delays in product availability, thereby securing a robust supply chain.

- Geopolitical environment: The nature of the industry makes it susceptible to trade conflicts between countries. Sanctions may impact the flow of material and components, leading to increased supply chain issues.

- Technological upgradation and talent – Workforce challenges: The industry involves a highly complex process and investments in research and development (R&D) and fabrication facilities. As chips become smaller in size, the need for innovation and skilled labour are major concerns and significant contributing factors in the space.

- Intellectual Property (IP) Protection: IP theft and cloning are challenges that can lead to revenue losses and reputational risks for organisations.

- Cyber risks: Frequency and severity of cyber losses have been at an all-time high following digitalisation. Cybersecurity poses a concern in disrupting the supply chain. Thus, ongoing monitoring of the software supply chain should be implemented to detect vulnerabilities and risks.

- Environmental, Social and Governance (ESG) risks: The industry’s high water and energy consumption, as well as the generation of hazardous waste, highlights the importance of adopting sustainable practices. Moreover, ESG risks can emerge due to the use of conflict minerals, poor labour practices, or insufficient oversight of the suppliers’ environmental practices.

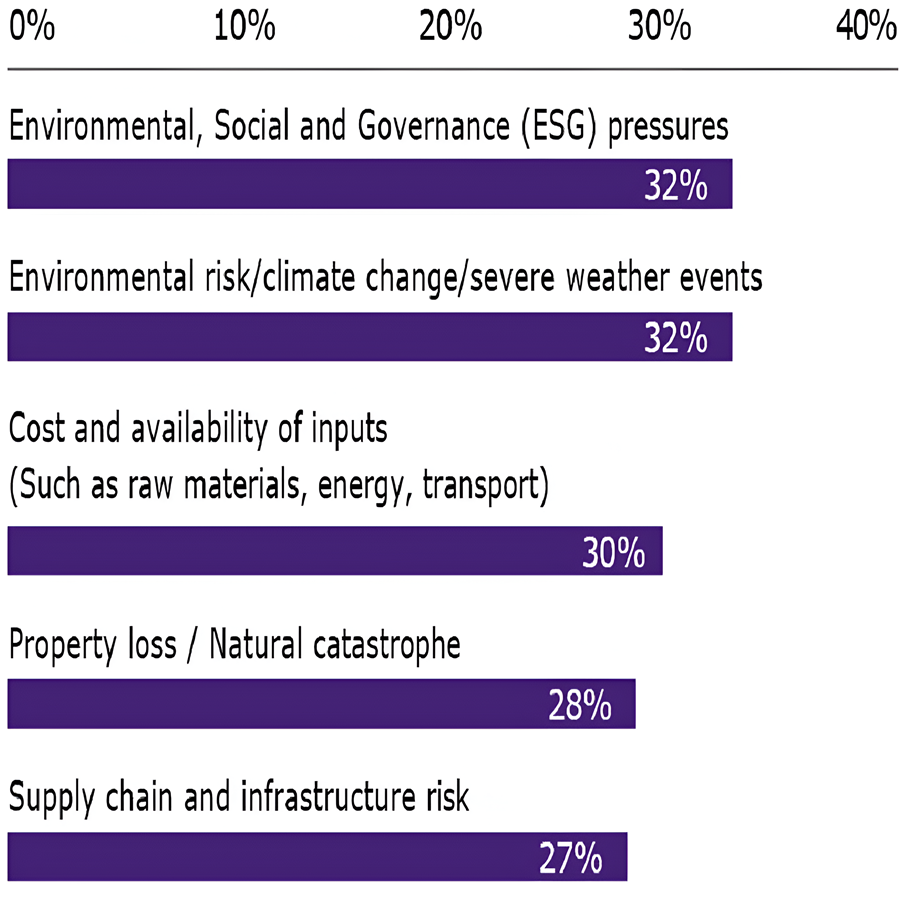

WTW’s semiconductor industry losses survey

WTW surveyed leaders in the semiconductor industry to gain insights into supply chain risks and challenges. The expansion of the semiconductor industry in India has brought a corresponding increase in risks to business supply chains.