In a recent meeting held by the Reserve Bank of India (RBI), lending rate of interest to the banks or the repo rate was increased by 40 basis points which is the first hike announced in nearly four years. This has pushed the 10-year bond yield to its highest levels in the last few years. Although this was an expected move to tackle the soaring inflationary pressures, the timing of the unscheduled announcement does come as a surprise.

It is to be noted that the annual inflation target until March 2026 has been set at 4% with a tolerance level of 2% on either side by the Government of India (GOI) and the RBI but the actual annual inflation rate has remained above 6% in the last three months. The annual inflation rate was 6.95% in March 2022 which is the highest since October 2020 and above the market forecasts of 6.35%. Surging commodity prices like consumer food price index of 7.68%, increase in prices of oils and fats by 18.79%, vegetables by 11.64%, fuel and light by 7.52%, clothing and footwear by 9.40%, etc. have contributed to the rise in consumer price index.

(Source: https://www.mospi.gov.in)

In order to set the inflation trajectory downwards again, it is expected that RBI may further increase the interest rates in the coming months as it aims to reduce the liquidity in the banking system. This trend is not specific to India and similar rising trends in yields are seen globally as well. For instance, the Federal Reserve Bank increased its benchmark interest rate by 50 basis points on the same day as RBI’s announcement and this is the biggest hike seen in two decades in the US to fight inflation.

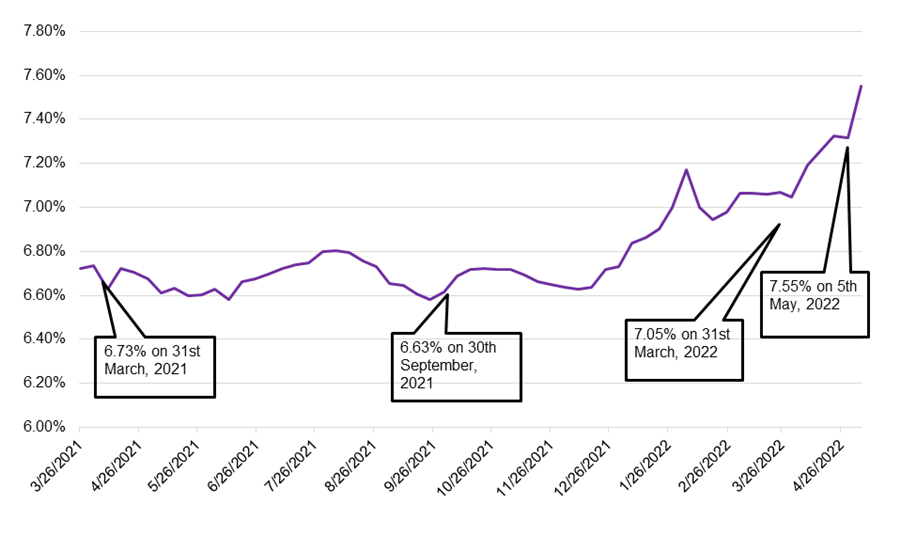

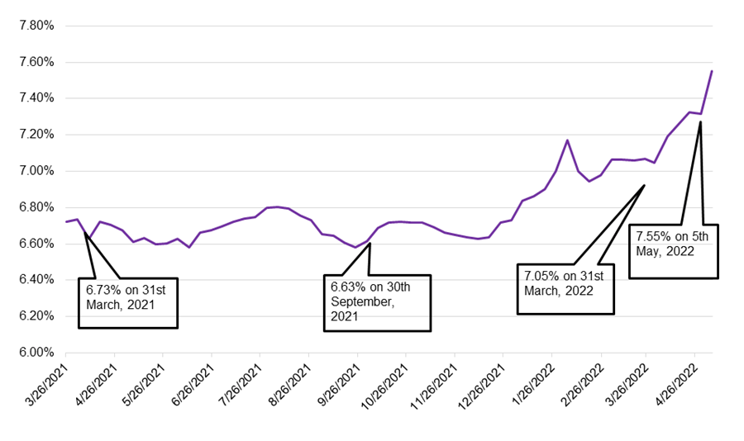

Given below is a snapshot of the Indian government bond yields over the last one year: