As we look further ahead into the downstream energy market, the losses sustained in early 2025 will continue to hang over the market mood as the risk of deterioration looms, but for buyers, there are reasons to be optimistic.

At a glance: Downstream energy insurance market trends

- The resurgence of soft market credits is the headline trend for 2025 so far, with long-term agreements (LTAs), prompt payment credits and no claims bonuses on offer.

- LTAs are providing opportunities for downstream energy companies to build some future certainty into their risk transfer programs.

- Capacity has increased modestly, but more significantly underwriters are willing to use more of their risk dollars on the best accounts.

- The market is seeing increasing competition for quality business and new premium.

- To maintain market share, (re)insurers are offering buyers more incentives to secure business.

- Rates are dropping, but are not in freefall.

- Evidencing risk engineering and high-quality information remain determining factors as to whether companies get a greater reduction.

Softening market conditions are likely to remain on course

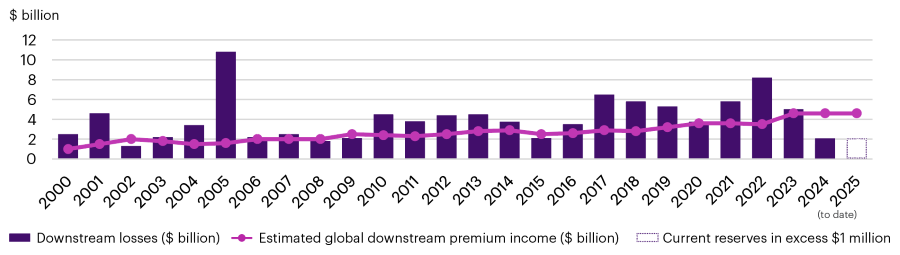

By the end of 2024, insurance buyers experienced a steady and meaningful market softening. With benign loss activity hovering around $1.417 billion resulting in a rare profitable year for the downstream market, there was a hope of a brighter outlook for underwriters.

But the tide turned. The market has had significant loss activity in Q1 2025 with $1.5 billion of potential losses, more than the entire 2024 year.

Despite this, our overriding prediction is that softening market conditions will remain on course throughout 2025. This could be derailed by several external global factors and further claims that could deteriorate loss ratios for the remainder of the year. In navigating this changing market, downstream energy companies can take advantage of soft market credits to withstand any volatility on the horizon, and others more focused on rates can optimize their insurance spend as insurers compete for top-tier business.

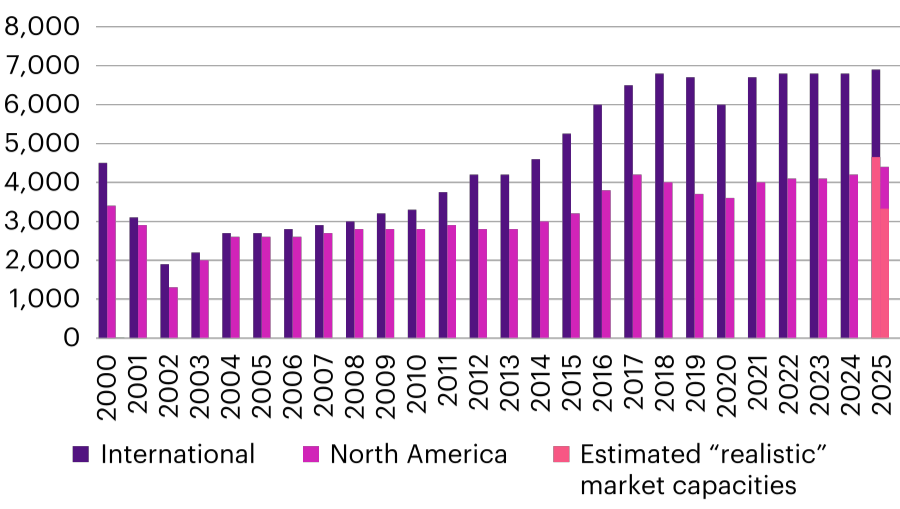

Working capacity is stable, but the appetite to use this capacity is the bigger story

New capacity continued to enter the downstream market in 2024, as a result, existing markets became more flexible with their pricing and overall appetite. Many carriers also increased their line sizes, making complex layered deals easier to place. In 2025, while working capacity for pure-play downstream oil and gas has increased only slightly, the drive to use the capacity has increased significantly. Meanwhile, the midstream market – particularly liquified natural gas – continues to attract big capacity with c.$150-200 million added since our last review, with some markets hungry to increase their market share and shake up the incumbent leaders.

Could 2025 losses change the course of the market?

The start of 2025 has shown a worsening loss record compared with 2024. While the 2024 loss activity was modest, significant loss potentials have already appeared in 2025. While these loss reserves are early approximations, the signs point to likely payouts being high. A further significant loss in the Asian market could compound these global figures, despite downstream energy companies making every effort to limit business interruption losses.

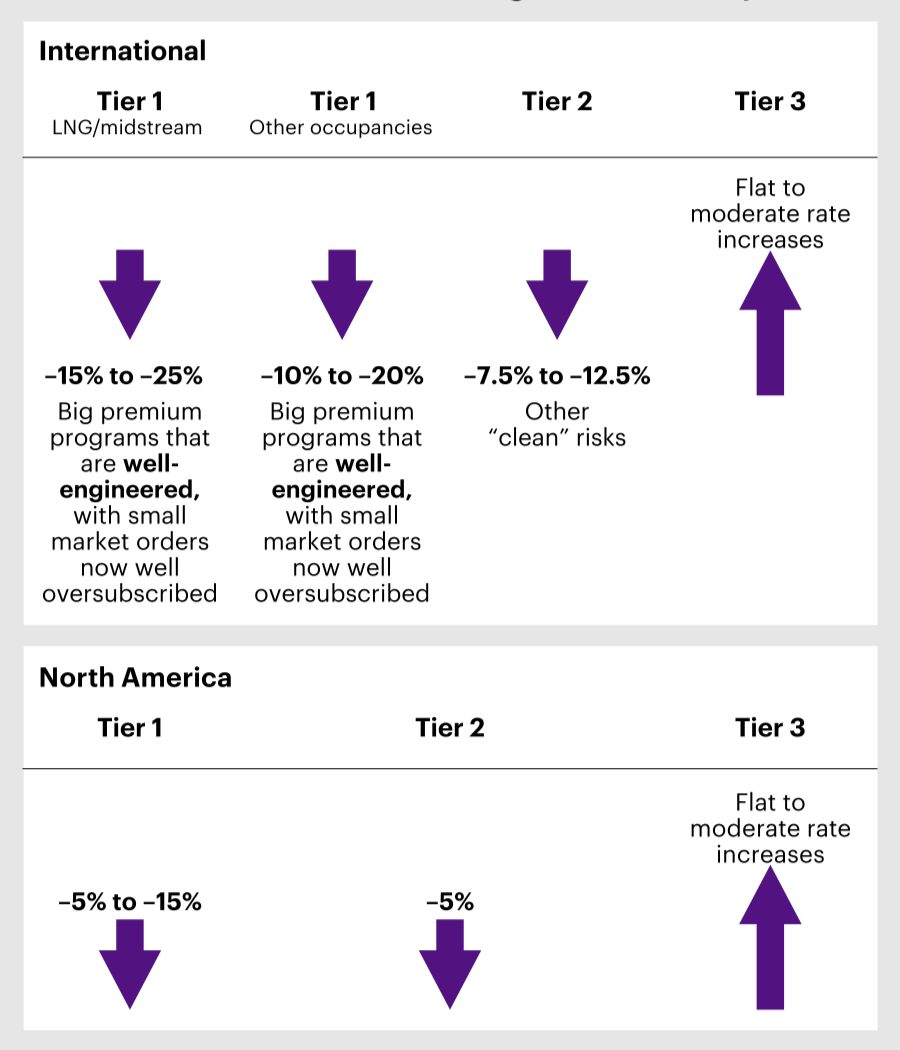

Soft market credits are making a resurgence in pricing negotiations

For now at least, the softening market sentiment looks set to remain, with high single-digit and low double-digit rate reductions the norm for most placements. As the market continues to soften, some well-engineered placements with large premiums and robust risk information could achieve up to 25% reductions. While markets are not yet yielding on terms and conditions, credits available in soft markets – such as long-term agreements and no-claims bonuses – are starting to appear on placements.

Table 1: Three-year deal advantages and disadvantages

A three-year deal can offer both advantages and disadvantages

| Advantages |

Considerations |

| Stability and security: It provides a longer period of security for both parties, ensuring a steady relationship. |

Lack of flexibility: Being locked into a longer-term agreement can restrict flexibility if circumstances change or the deal is not beneficial over time. |

| Potential cost savings: Often, a longer-term commitment can result in cost savings or better rates compared to shorter contracts. |

Commitment risks: LTAs may leave clients tied into terms that are no longer favourable. Insurers on the other hand will have a number of caveats allowing them to break the LTA such as loss ratio triggers, material risk changes and treaty movements. |

| Time to develop relationships: It allows for the development of deeper relationships and understanding, which can be beneficial. |

Potential for complacency: Both parties might become complacent in their performance or service delivery, and pressure to strive for continued improvements could diminish. |

Downstream energy companies need to consider the value of these soft market credits. For companies seeking stability and security, an LTA could be a valuable option to provide certainty of premium spend, particularly considering the uncertainty created by the recent market losses. It is possible to hedge your bets by placing a proportion of the risk on an LTA, giving a level of certainty, while keeping the remainder of the placement renewing annually which may benefit from any further rate softening. For companies whose primary focus is rate optimization, LTAs might not be as appealing if there are potential rate reductions in subsequent years.

Insurance buyers are in a strong negotiating position

Heightened market competition, particularly for the most favoured risks, places buyers in a strong position to achieve competitive terms, and to lock these savings in for multiple years as part of a considered and data-driven risk strategy.

Contact our specialists to find out how a triad of risk engineering, analytics and broking can make a meaningful difference to what you can achieve in the year ahead.