Strong pension fund positions and generous benefits – but limited employee awareness of SLI pension plans

SLI Pension Benchmarking Study 2025

September 3, 2025

ZURICH, GENEVA, LAUSANNE, September 3, 2025 – Swiss pension funds are currently in very solid financial shape, and companies included in the Swiss Leader Index (SLI) continue to provide pension benefits at the upper end of the market, significantly above the BVG minimum benefits. This is positive news for employees and a strong signal in support for the Swiss retirement system. For the first time, this year’s study by WTW also asked companies about employees’ awareness of their occupational pension benefits. The results show clear room for improvement as awareness levels are low, and companies could do more to inform, engage and support their employees.

With the aim of comparing pension plans and the resulting benefits, WTW regularly conducts this SLI Benchmarking Study. It analyses the main features of the Swiss pension plans of the companies included in the Swiss Leader Index (SLI) and compares the effective level of benefits. In 2025, 25 of the 30 companies included in the index are included in the study.

Strong financial performance over five years

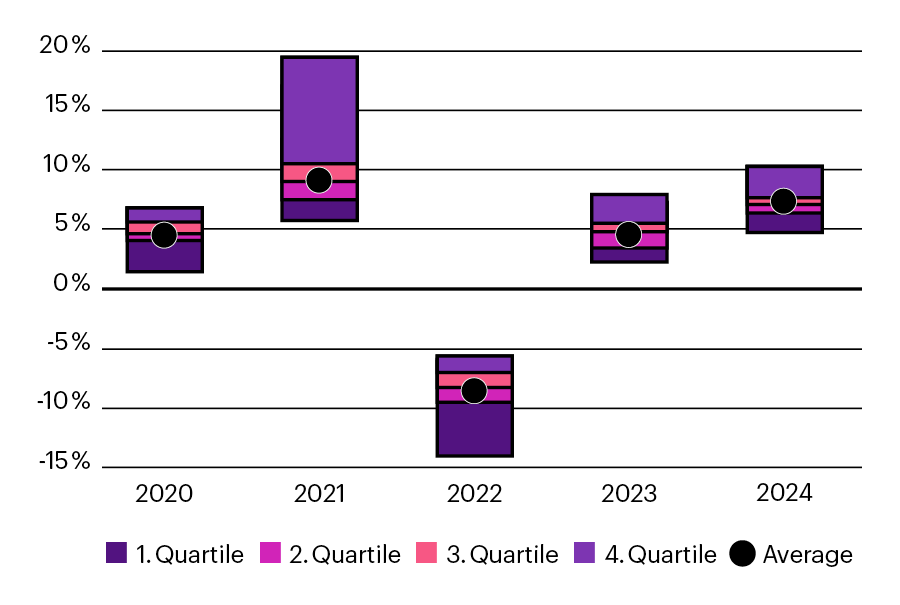

Most Swiss pension funds find themselves in a robust financial position supported by solid investment performance over the past five years. The SLI group achieved an average return of 3.4% per annum, which has contributed significantly to current fund stability. The chart below illustrates the annual investment returns of participating companies from 2020 to 2024. It highlights the market volatility over this period, showing strong positive returns in 2021 and significant losses in 2022, while also demonstrating an overall stable trend.

Historical Asset Returns

This graph shows the historical asset returns from 2020 to 2024.

Technical interest rates have stabilised

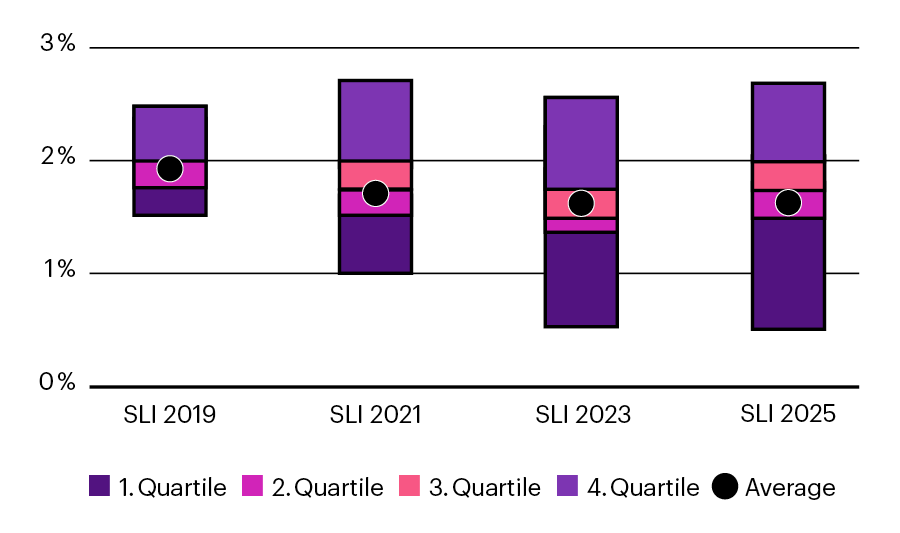

Over the past six years, the technical interest rates, which determine how pension liabilities are calculated, have stabilised at 1.5% and 2.0% for most SLI pension funds. As shown in the chart below, this rate stability has helped reduce pressure on liabilities and allowed more of the investment returns to be passed on to plan members via credited interest.

Technical Interest Rates (in %)

This graph shows the technical interest rates from 2019 to 2025.

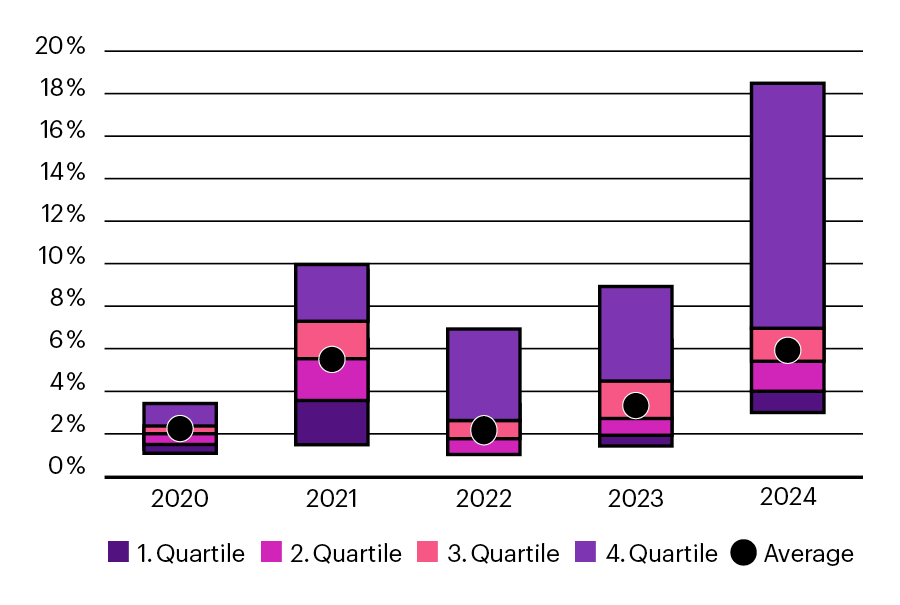

The study also found that credited interest rates across the SLI group have been close to actual investment returns. This indicates that funds have not needed to use returns primarily to cover increasing liabilities – a strong sign of financial resilience. In 2024, the spread of credited interest was particularly wide, with top rates exceeding 18%.

Historical Interest Crediting Rates

This graph shows the historical interest crediting rates from 2020 to 2024.

High benefits but notable differences between SLI companies

Taking a pension is a key part of long-term financial planning. It provides employees with a guaranteed income at retirement, offering peace of mind and financial stability after their working years. However, the level of pension benefits depends on several factors -most notably, the contributions, the interest credited to the retirement savings balance, and the conversion rate applied at retirement age.

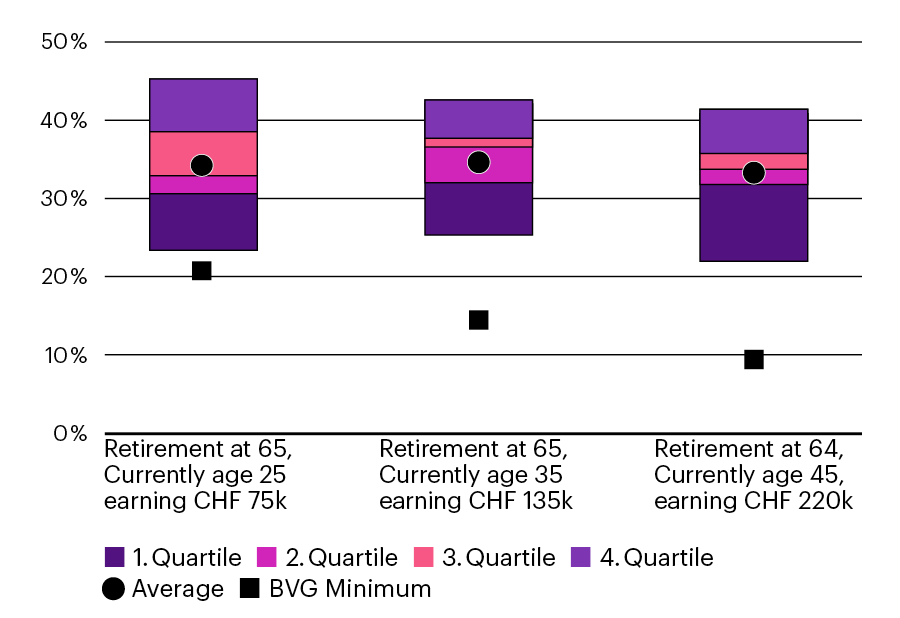

The SLI study highlights that while all companies offer high pension benefits, there are significant differences in pension outcomes between them. As in previous studies, WTW defined three employee profiles and calculated their projected pension amount as a percentage of base salary at retirement.

As seen in the chart below, all companies provide pension benefits well above the BVG minimum benefits to their employees, some to a very considerable extent. For profile 1 joining aged 25, completing their full career with the company, the lowest pension level for the SLI group is around 23% of base salary at retirement, whereas the highest pension level is around 46% of base salary. Hence, the most generous company pension arrangement is expected to provide around twice as much pension income as the least generous company and almost 2.2 times more than the BVG minimum benefits. For joiners at a later stage of their career (profiles 2 and 3) there are also significant differences, which reflect differences in generosity just over the remaining portion of their careers to retirement.

Pension Levels at Retirement

(as a % of Base Salary at Retirement)

This graph shows the pension levels at retirement at 65.

Retirement pensions are a critical component of post-career financial security. It is essential that employees understand the value of their pension benefits, as these play a critical role in ensuring financial well-being during retirement. Throughout their careers, employees should take proactive steps to save and plan for retirement, making informed decisions to safeguard their long-term financial well-being.

Employees awareness remains low on the benefits being provided

Despite the strength of the benefits offered, almost half of the companies in this study believe that their employees only have a basic understanding of the pension arrangements – essentially knowing there are pension benefits provided but not knowing how valuable they are.

To address this gap in awareness, WTW recommends that companies take a more proactive and strategic approach to communication. This includes regularly informing employees about the structure, risk and retirement benefits, and opportunities within their occupational pension plans. Particular emphasis should be placed on individual design options, which must be clearly explained to ensure employees can make informed choices.

In addition, companies are encouraged to use benchmarking studies to compare their pension offerings with those of selected competitors, helping both employers and employees understand the relative value of their plans. Finally, WTW stresses the importance of consistent and transparent communication, which both strengthens employees’ understanding and reinforces their sense of being supported and valued by their employer. Effective communication fosters greater engagement, helps employees recognise the value of their benefits, and ultimately contributes to their financial security and overall satisfaction.

About WTW

At WTW (NASDAQ: WTW), we provide data-driven, insight-led solutions in the areas of people, risk and capital. Leveraging the global view and local expertise of our colleagues serving 140 countries and markets, we help organisations sharpen their strategy, enhance organisational resilience, motivate their workforce and maximise performance.

Working shoulder to shoulder with our clients, we uncover opportunities for sustainable success – and provide perspective that moves you.

In Switzerland WTW is based with offices in Zurich, Geneva and Lausanne.