International Pension Plans (IPPs) and International Savings Plans (ISPs) are used by multinational employers to provide retirement or savings benefits. These plans were originally set up for internationally mobile employees who could not be retained in their home country retirement plans or for whom more traditional local (host) solutions weren't appropriate or available. Nowadays, these plans are also offered to local employees across various markets.

WTW’s survey of plan providers captures details from large and midsize multinational companies across a wide range of industry sectors to gain insights into:

- The geographical coverage of IPPs and ISPs and the vehicles used to establish them;

- Membership criteria and plan design elements;

- The integration of environmental, social and governance (ESG) considerations within these plans.

Key Findings

- Market demand: 16% of IPPs and ISPs were established in the last five years, with banking and finance showing significant interest, representing one in seven of these new plans.

- Employees’ savings protection: There is an increasing trend to extend eligibility of IPPs and ISPs to local employees, particularly in countries operating in challenging political and economic circumstances. One in four IPPs and ISPs set up in the last five years provide these benefits to local employees. Trusts prevail as the preferred vehicle to safeguard employees’ savings and protect them from any local turbulence, including high levels of inflation.

- ESG investments: Plan sponsors’ interest in reviewing fund ranges for ESG considerations (including diversity, equity and inclusion audits) is on the rise, with nine out of 11 providers reporting an increase in switching to ESG funds.

- Governance: The level of governance and oversight around IPPs and ISPs continues to be relatively low, despite its importance during periods of uncertainty and economic turmoil.

Market Demand

The survey reveals that 142 IPPs and ISPs were established over the last five years, with the highest concentration in banking and finance accounting for some 15% of these plans. Other sectors attracting significant interest include oil and gas (12%), non-profit organizations (11%) and engineering and power (11%). Most are described as global (Figure 1), accommodating members from diverse geographies and nationalities, with over three in four IPPs/ISPs domiciled in either Isle of Man or Luxembourg. We also see a marked interest to set up new IPPs or ISPs exclusively for local employees, with more than one in four plans set up over the last five years to cover local employees across various markets.

Figure 1: Coverage of plans set up in last 5 years

Safeguarding employee savings

As demand for IPPs and ISPs increases, often driven by including wider geographical coverage, other challenges can arise. Economic and political instability in many countries, along with rising inflation have created many challenges for employers looking to give employees stable pension/savings arrangements. Since 2020, there have been 18 sovereign defaults in ten countries. High inflation and rising costs of borrowing due to high interest rates have made it much harder for many nations to repay foreign loans or to raise funds, further adding to the likelihood of defaults. This presents a challenge for employers that have local pension arrangements in these countries, especially when these local pensions are invested locally.

IPPs and ISPs can be used to provide a more secure vehicle and deliver better pension outcomes with access to global investment funds, thereby reducing exposure to local high-risk markets. Of the IPPs and ISPs surveyed, one in eight (126 plans) are offered to local employees in these countries. The number of plans that cover countries that might be viewed as operating in challenging circumstances is on the rise and has more than doubled in the last five years (Figure 2). A major advantage of IPPs and ISPs is that hard currencies are used, such as USD, GBP and EUR, which protect members from currency devaluation. Most of these plans are set up as trusts domiciled in Isle of Man, Jersey and Guernsey and provide global coverage.

Figure 2: "Plans offered in countries operating in challenging circumstances"

In 2019, 54 plans were offered in countries with challenging circumstances. Since then, this number more than doubled in 2024, to 126 plans. In a high inflation environment, where interest rates and cost of living is high, it's important to ensure that the fund range available to members is wide enough to provide sufficient choices. Where the fund range has been limited, efforts have been made to diversify the fund range to include asset classes such as real estate, commodities, gold, index-linked bonds and equities, which offer some level of protection against inflationary pressures. Within an asset class including emerging markets, which tend to keep pace with inflation, are also considered. We have observed most providers are able to implement these changes subject to the agreement of trustees.

Increase in IPPs and ISPs in countries with challenging political and economic circumstances

In 2023, countries most affected by currency devaluations included Angola, Argentina, Egypt, Lebanon, Turkey and Zimbabwe. Consequently, there has been an increase in IPPs and ISPs offered to employees in such countries because IPPs and ISPs invested in hard currencies (e.g., USD, EUR) tend to be less impacted by currency devaluations and economic fluctuations. We have seen an increase in demand in locations such as Lebanon, Ukraine and Zimbabwe for IPPs and ISPs for this very reason.

The graph below (Figure 3) shows the number of IPPs and ISPs offered in 2023 and 2024 in countries with challenging political and economic circumstances.

ESG investments, including diversity, equity and inclusion (DEI) considerations

Environmental, social and governance (ESG) has become an important consideration among fiduciaries and governance committees that oversee IPPs and ISPs.

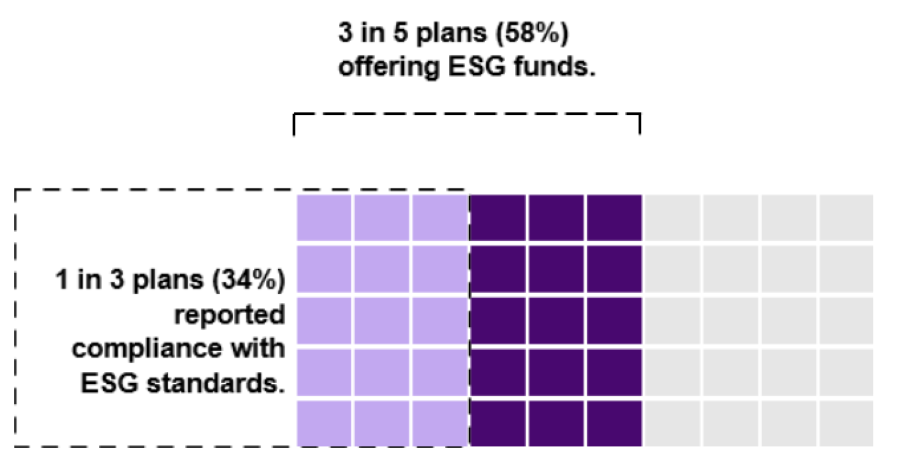

In our survey, around three in five plans (58%) offer ESG funds in their investment range, out of which one in four plans (34%) reported compliance with minimum standards for achieving ESG targets. Plan sponsors’ interest in reviewing fund ranges for ESG considerations (including DEI audits) is on the rise, with nine out of 11 providers reporting an increase in switching to ESG funds (figure 4).

Figure 4: Prevalence of ESG funds

Providers are prioritizing diversity, equity and inclusion (DEI) initiatives within IPPs and ISPs, recognizing the importance of fostering greater diversity, inclusivity and equity among participants.

The 2024 survey also shows that gender-neutral plan designs are becoming more prevalent, and providers are actively engaging with sponsors and employers to understand their DEI philosophy and objectives. They also run periodic communication campaigns about the plans and members’ options to enable informed decision-making.

Employee financial wellbeing is another growing area of focus for employers. Provider offerings for members’ financial wellbeing include tools to assess attitude to risk, online budgeting and projection tools and financial education workshops. Most providers have in-house teams to deliver these offerings to plan members. Providers also provide communication and educate members on the impact of exiting from their plans at the wrong time; many also may allow early, partial or hardship withdrawals.

The rise in Shariah funds within the realm of sustainable investments

Shariah funds are a subset of the responsible investment framework sharing similarities with the ESG criteria, particularly the aspects related to socially responsible investing. This incorporates a requirement to exclude investments viewed as non-Shariah, for example, gambling, tobacco, alcohol, guns and ammunition.

We have observed an increase in situations where prospective members of IPPs and ISPs have been unable to participate in plans, due to an absence of investment funds that meet their personal or religious principles. This has led to a rise in IPPs and ISPs incorporating more choices across broader asset classes. This can be expected to continue to increase in popularity in the years ahead and is not just relevant to IPPs and ISPs, but domestic pensions as well.

ESG discussions with fiduciaries often result in changes to fund ranges, including the introduction of ESG funds (which might be a Global Equity option that screens out certain industries like coal mining, guns and ammunition). Sometimes this includes Shariah funds (usually in Global Equity but may also include Sukuk and Money Market options).

This year’s survey highlights that plan sponsors interest in reviewing fund ranges for ESG considerations (including DEI audits) remains high, with nine out of eleven providers reporting an increase in switching to ESG funds, compared to eight out of ten providers last year.

Governance

The IPP and ISP market continues to develop more robust governance and oversight frameworks, but currently only two in five plans (Figure 6) indicate they report to a governance committee. IPPs and ISPs average around 50 members or fewer and sponsors may view the IPP as being immaterial (too small) for DC oversight. However, recent market volatility has affected fund values, emphasizing the importance of robust governance structures in monitoring plan performance and recalibrating the design or fund options at specific intervals to ensure that the plan is meeting its objectives, and that the governance framework is effective, efficient and compliant with regulatory requirements. Emerging themes like ESG and inflation protection may also speed up the need to have strong governance and oversight around IPPs and ISPs.

Providers are stepping in to address the governance gap in this market; over three-quarters of providers are actively involved in revising or establishing governance framework structures, recognizing the need for a more structured approach. Also, over half of the providers are contributing to the enhancement of governance through training and education initiatives tailored for trustees and members of these small-group plans.

About the survey

The International Pension Plan Survey 2024 is the 16th edition of the annual survey conducted by WTW. This year, we reported on 1028 plans sponsored by 960 organizations. Total assets under management in this year’s survey is estimated to be around $19.5 billion. The sample comprises large and midsize multinational employers across a wide range of industry sectors.