As insurance coverages and perils become more interconnected, forward-looking climate models will be critical to provide a more accurate view of the extent to which climate change is intensifying natural catastrophes.

2023 was the planet’s warmest year since records began in 1850, according to analysis by the National Oceanic and Atmospheric Administration (NOAA).[1] The NOAA reported that the temperature of the Earth’s land and ocean surface last year was 1.18°C above the 20th century average. The past decade contains the 10 warmest years since 1850 and the average global temperature for 2023 exceeded the pre-industrial (1850-1900) average by 1.35°C.

The NOAA have estimated that there is a one-in-three chance that 2024 will be warmer than 2023, and a 99% chance that 2024 will rank among the top five warmest years.

A year of record heat temperatures

Record ocean temperatures: The oceans store 90% of the excess heat in the Earth’s system, making ocean heat content a key climate indicator. The amount of heat stored in the upper 2,000 meters of the ocean in 2023 was the highest on record as reported by the NOAA. This has been tracked globally since 1958 and has seen a steady upward trend since approximately 1970. The five highest values have occurred in the last five years. Warming of ocean water raises global sea levels due to the thermal expansion of warm water, combined with the additional water from melting glaciers, the rising sea levels threaten natural ecosystems and human structures on global coastlines. Warmer oceans also fuel stronger hurricanes, increasing the risk that they could undergo rapid intensification. This could result in significant human and economic losses. Coral reef bleaching is exacerbated, which will also impact marine ecosystems and those who depend on them.

Reduced polar sea ice: The 2023 annual Antarctic Sea ice extent was the lowest on record, with an average 3.8 million square miles. The Arctic Sea ice extent averaged 4 million square miles in 2023, which is amongst the 10 lowest years on record. As warming temperatures gradually melt sea ice over time, this reduces the number of bright surfaces to reflect sunlight back into the atmosphere, causing more solar energy to be absorbed at the surface which leads to ocean temperatures rising further. The changes in the extent of sea ice at the polar caps disrupts normal ocean circulation leading to changes in global climate.

Warmest December on record: 2023 saw the highest global surface temperatures for December on record, with an increase of 1.43°C above the 20th century average.

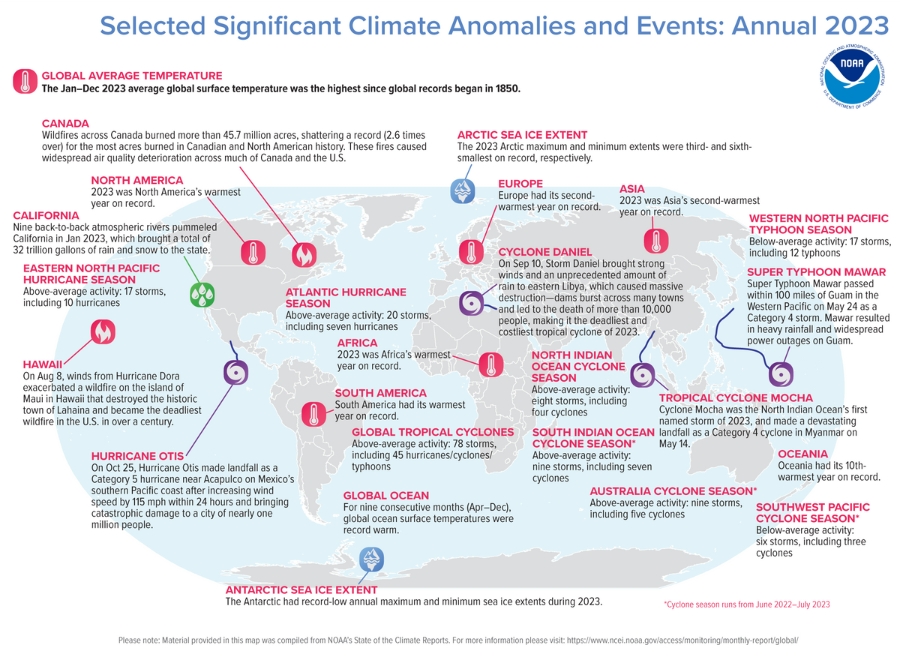

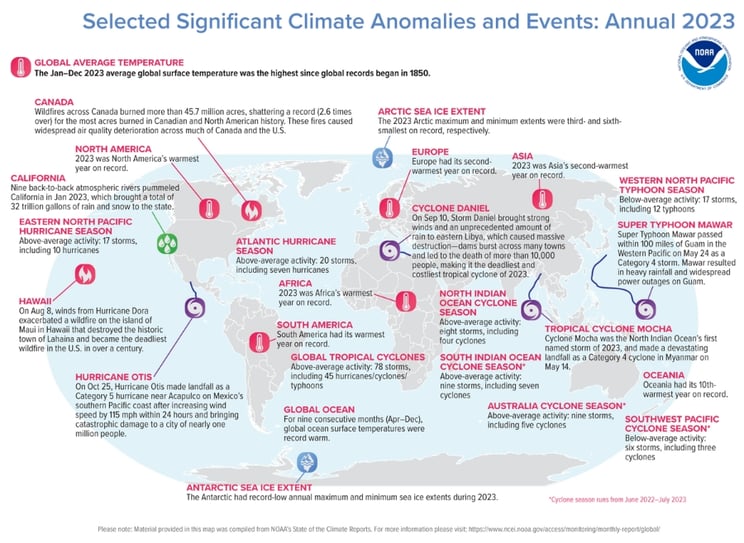

The below image depicts key natural catastrophe events across the globe in 2023.

Significant Climate Anomalies and Events: Annual 2023

NOAA National Centers for Environmental Information, Monthly Global Climate Report for Annual 2023, published online January 2024, retrieved on 15th February 2024 from Annual 2023 Global Climate Report

Significant Climate Anomalies and Events: Annual 2023

Significant Climate Anomalies and Events: Annual 2023

NOAA National Centers for Environmental Information, Monthly Global Climate Report for Annual 2023, published online January 2024, retrieved on 15th February 2024 from Annual 2023 Global Climate Report

Earth on brink of climate tipping points

The IPCC (Intergovernmental Panel on Climate Change) has identified several so-called ‘tipping points of climate change[2], critical thresholds in a system that, if exceeded, could lead to irreversible consequences. Crossing these tipping points may lead to a step change in the frequency and severity of natural catastrophes such as those seen in 2023.

As early as 15 years ago, there was a consensus amongst many academics and scientists that most tipping points could be reached in the event of a 4°C increase in global temperatures. Now recent assessments reveal that surpassing the 1.5°C threshold will trigger multiple tipping points, further exacerbating the impact of climate change and biodiversity even if current temperature rise targets are met.

The most likely tipping points to be crossed this century due to anthropogenic activity are: warming of the Arctic ice sheet; thawing of the permafrost below the Earth’s surface; ocean circulation and currents driven by differences in the density of water (Atlantic Meridional Overturning Circulation); weather-related events forcing relocation; Amazon rainforests and their ability to absorb greenhouse gases; the melting of the Antarctic ice sheets; and coral reef die-offs impacting nitrogen and other nutrients for marine food chains.

In the recent report ‘The Emperor’s New Climate Scenarios’,[3] the Institute and Faculty of Actuaries (IFoA) warns that current climate-change scenario modeling techniques still exclude many of these more severe impacts that we can expect from climate change – they simply do not exist or are not well represented in models and methods that we use today.

Consequently, results emerging from our generally adopted methods are considered to be benign, and even improbable in some cases. Herein lies the danger: results may provide “in the moment” comfort to stakeholders, but will be particularly perilous for key decision makers especially as the aggregation of benign results and misplaced confidence may lead to erroneous management actions. Indeed, insurers’ financial stability can’t just be analyzed solely through the lens of its insurance portfolio in isolation, but rather must be observed as it relates to the wider financial system and its connection with the real economy.

With risk oversight of activities conducted by the first line of defense (LOD), such as the underwriting business and corporate functions, Chief Risk Officers and Heads of Exposure Management (the latter often crossing into the world of risk management) are increasingly playing a critical role in providing results and guidance to Boards and Risk Committees vis-à-vis climate attestations. Not only are these functions managing complex risks and decisions alongside fellow first line teams, they often need to draw upon external insights and metrics that provide top line management with perspectives and validation on strategic business risks. In managing complex risks, exposure management aims to measure downside but also enable the business to make the ‘correct’ management actions, with risk–reward trade-offs to capture the upside. Climate change risk is not so different.

It is a delicate balance. Underestimating systemic and complex risks could mean over insuring or investing in classes that deviate from a company’s vision and strategy, resulting in unwanted surprises.

Materiality and proportionality – one size does not fit all

Climate change - complex, nuanced and characterized by uncertainty – warrants the need for forward-looking climate models, especially at a time when insurance coverages and perils are becoming more interconnected.

To be effective, CROs alongside exposure managers are required to address material limitations and uncertainties of not only probabilistic modeling but also scenario modeling. Climate change requires a new lens through which to view materiality and proportionality, alongside current methods. The global risk landscape is more complex and interconnected and the potential for disasters to cascade through systems is increasing with the impacts having greater geographical, social and temporal reach. The ‘Emperor’s New Climate Scenarios’ coupled with a climate specific materiality and proportionality lens would provide a more accurate view of the extent to which climate change is intensifying natural catastrophes, both today and in the future.

Bridging the gap

To adopt a purpose-built materiality framework for climate change, three practical and critical elements should be considered:

01

Culture and buy in

The climate engagement between Boards, 1LOD and 2LOD should be clearer, documented and well structured to assist the business. Expertise bottlenecks and scope creep in functional roles (non-climate roles incorporating climate responsibilities) are likely to bring about erroneous positions on climate. A top-down strategy regarding climate change, typically adopted by many companies, should be complemented by a commitment to share information from functions. This ensures key underwriting, pricing and claims messages (quantitative and qualitative) are communicated up and across the business to continually measure the appropriateness of climate change methods with board-approved risk appetites and wider ESG strategies.

Feedback loops are enablers and therefore provide a positive shift from focusing on the past and more towards a current and forward-looking assessment of climate impacts. Exploring different scenarios and counterfactuals[4] helps to understand the uncertainties and the gaps to address accordingly.

02

Models and methods

Models that are appropriate for an insurer’s own business must be proportionately validated to address strengths, limitations and weaknesses, and then logged for future review. Scenario modeling is an important component of the risk management toolkit. Therefore investigating extreme but plausible scenarios enables insurers to establish how different combinations of aggregations could impact the future solvency of a financial entity and what action could be taken to mitigate this. Measured against a current ‘view of the world' taxonomy of plausible catastrophe threats – including tipping points that have the potential to cause damage and disruption to social and economic systems – scenario modeling should now be a standard tool within an insurer’s armory.

In the context of climate change, scenario modeling enables financial institutions and regulators to investigate the impact of different climate futures, which is important given the challenges we face. At the same time, it is essential that firms address the material limitations of models and scenarios and move towards normative climate scenarios[5] that not only recognize the catastrophic impact of a hot-house world, but help insurers manage portfolios through a less exploratory lens.

03

Validation

The techniques insurers and underwriters use today are tried and tested and most remain fit for purpose. But the world is changing. So rather than discard what

an insurer already has in place, they should instead draw on external opinions and ideas that enhance the understanding they have already developed. By embracing more sophisticated methods in which new insights are incorporated into underwriting, claims, exposure and risk management, combined with lessons learned on recent natural catastrophes, insurers will be better placed to measure and respond to the climate challenge.

How can WTW help

WTW’s multi-disciplinary team can support firms with climate risk and exposure management with professionals embedded within the wider P&C consulting team. WTW can support all areas of an organization in adopting the most suitable framework, embedding methods and upskilling 2LOD and 1LOD for managing climate change.